Strong Demand: JK Paper recorded its highest ever quarterly Consolidated Turnover in Q2

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

JK Paper reports a 134 percent jump in Q3 profit after tax, maintain its leadership position in Cut –size office paper

"Paper Industry will no longer be in the traditional 3-5 years of cycles": FPTA

TNPL will focus on increasing its market share in Virgin Fiber grades; Intends to strengthen the dealer network

A new double wire paper mill of Kraft paper productions started in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

Genus Paper & Boards acquired NS Paper; focus on differentiation, innovation, and automation

CPPRI: Paper Industry contributes Rs. 8000 Crores to the National exchequer with a turnover of Rs.70000 Crores

Satia Industries: better product mix and higher sales realization drive increased revenue in Q2FY23

Vishal Paper Mills to Produce Multi Layered Card Board Material for Packaging

Paper mills in Morbi face a 50% drop in demand amid the ceramic industry closure; kraft paper prices may see intense price-cutting competition

Printers demand single slab of 12% GST on all converted/printed products: AIFMP

Paper Market scenario of WPP, Coated, and Packaging Boards, and MIP impact: Insights by Mr. Bhavesh Gala

“Paper mills are supplying at 0% GST but with a increased price to the extent of their Input credit loss,” says Mr. Shailendra Gala of Navneet Education

“FCBM urges brands to recognize the value addition by corrugators and ensure equitable pricing,” says Mr. T. M. Raghavan of FCBM

Seshasayee Paper to raise capacity from 2.55 to 4 lakh tonnes, backed by a Rs 750–800 crore investment plan over the next two years

It is estimated that USD10B to USD20B worth of single-use plastic packaging will convert to molded fiber, ZUME

EBMA: With books exempt from GST, imported finished books enter India tax-free; notebook prices may climb 15–20% with GST hike

Muzaffarnagar gets a new capacity of Tissue Paper and MG Poster paper

BioCNG from paper mill effluent: India’s & Asia’s First Paper mill, Sainsons Paper to Produce & Sell CBG/BioCNG From Waste Water

Barrier-Coated Paper, RTE Demand, and E-Commerce: Experts Predict Paper-Based Packaging Market to Reach USD 46 Billion by 2030

Indian Pulp and Paper Industry: Opportunities, Growth Drivers, Challenges, and Outlook

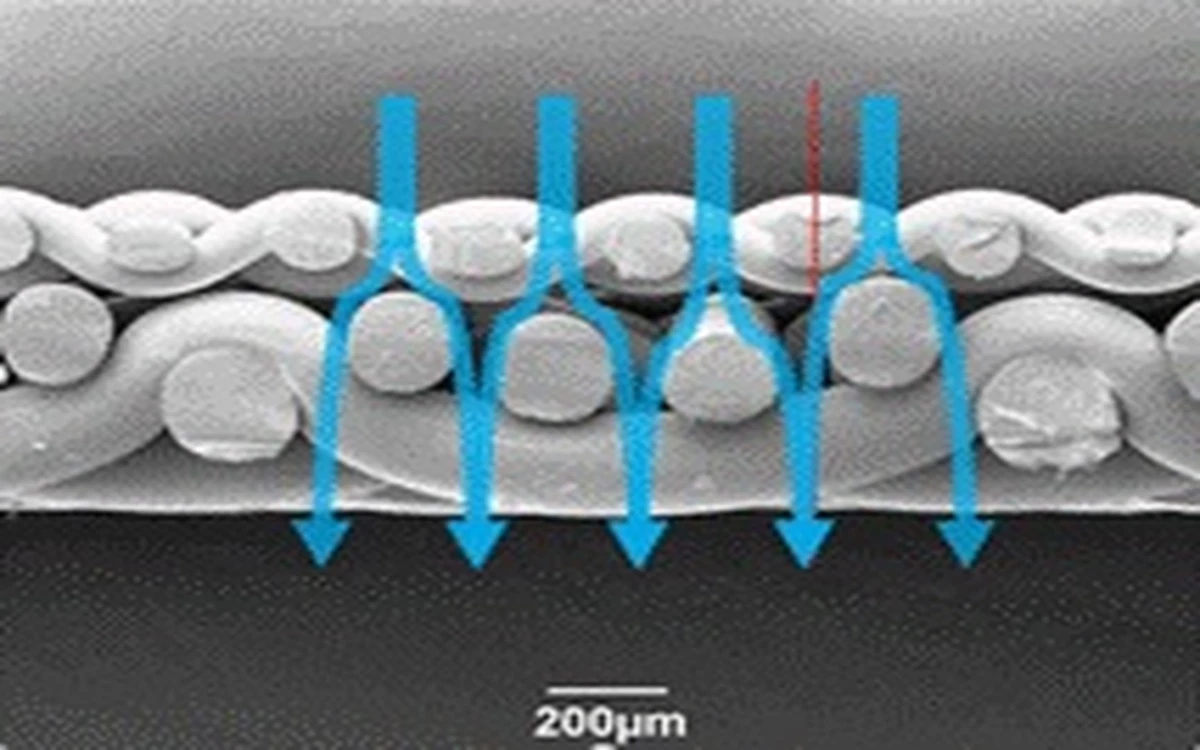

Fiber Recovery And Water Reuse in Paper Mills Through Closed Water Loop- A need of hour

The Pulp and Paper Times, August 2016 Issue

The Pulp and Paper Times: Volume 1 issue 6

The Pulp and Paper Times: Volume 2 issue 1

The Pulp and Paper Times : Volume 3 Issue 2

The Pulp and Paper Times: Volume 4, Issue 5

The Pulp and Paper Times Magazine : Volume 5, Issue 2

The Pulp and Paper Times Magazine : Volume 6, Issue 1

Sappi is a global diversified wood fibre company focused on providing dissolving wood pulp, packaging and speciality papers, graphic papers, as well as biomaterials and biochemicals to our direct and indirect customer base across more than 150 countries. Here is the interview of Mr Steve, CEO, SPPI

Q: Debt levels increased last year while profitability declined, resulting in higher leverage – what is Sappi doing about this?

As market conditions worsened and the outlook for a recovery faded, we took decisive action on a number of fronts to minimise the rise in debt levels and lessen the impact of the increased leverage. At the start of the year, capital expenditure in 2019 was expected to be US$590 million. Through a careful process of re-evaluating the priority and timing of various projects, total spend for the year was reduced to US$471 million. We have also adjusted down our expansionary capital spending plans for 2020, effectively reducing this to projects under way or already committed. Maintenance, safety and environmental spend were unaffected as we seek to ensure the sustainability of the company. Production downtime was taken as required in the graphics paper segment in order to minimise inventory levels and working capital, resulting in strong cash generation in the latter part of the year.

We continuously evaluate opportunities to extend debt maturities and lower finance costs. We refinanced the 2022 Euro bond early in the year, lowering the interest charge and extending maturities. This has meant we have a comfortable liquidity position, with no major maturities due before 2023, a low average interest rate and flexible liquidity from cash on hand and undrawn revolving credit facilities. In the fourth quarter, we renegotiated the leverage covenant for our European revolving credit facility and some of our bank term debt, due to current market uncertainty and particularly with regards DWP pricing, to provide further headroom. This renegotiation resulted in increased headroom over the expected peak leverage periods, moving the maximum leverage level from 3.75 times net debt:EBITDA to 4.5 times.

Q: You acquired the Matane Mill just after year-end while deliberately reducing capital expenditure levels – what was the rationale?

Our packaging and speciality operations in the United States and Europe are typically less in integrated pulp than our graphic paper business, and this brings higher pulp cost and volatility in earnings through a pulp cycle. Additionally, our paperboard machines benefit from using high-yield pulp, where supply is more constrained than for kraft hardwood or softwood pulps. We thus had a medium term strategy to build our own high-yield pulp mill at Somerset to lower costs for our packaging businesses, reduce volatility in earnings and secure this key raw material. Matane Mill was a major supplier of high-yield pulp – when it came onto the market, we weighed up the benefits of purchasing a mill at significantly less than replacement cost and securing a key raw material against the desire to reduce leverage. We believe we purchased the mill at an attractive valuation, and the acquisition will benefit our growing packaging and speciality business. Our internal consumption of pulp from the mill will increase as we ramp up paperboard production at both Somerset and Maastricht Mills in coming years. However, we will continue to supply the high-yield market.

"The Need to develop more environmentally friendly solutions, derived from renewable materials, will drive increasing market share for viscose, which is derived from dissolving wood pulp."

Q: Dissolving wood pulp prices, a key determinant of Sappi's profitability, declined by almost a third since the end of last year. Does this change your outlook for this critical key segment of the business?

We believe the fundamental attractiveness of the DWP market remains intact. As global textile demand grows, driven by population growth, fashion and rising wealth in developing economies, the need to develop more environmentally friendly solutions, derived from renewable materials that do not threaten food security or aquatic systems, will drive increasing market share for viscose, which is derived from dissolving wood pulp. Despite the challenges in the past year, VSF demand still grew by 6%, with pricing influenced by a confluence of factors largely external to the dissolving wood supply and demand dynamics. Weakening economies in various parts of the world, the impact of United States/China trade tariffs on textile production and sales and the rapid increase in VSF capacity over the past two years have led to a situation where VSF mills are running at very low operating rates and depressed VSF selling prices are forcing DWP prices lower. With no alternative outlet due to the concurrently weak paper pulp market, DWP swing producers have now become price takers. We believe that these circumstances will steadily change as the current situation is unsustainable as a large proportion of VSF mills and a significant proportion of DWP mills are generating cash losses at prevailing pricing levels.

Q: Global graphic paper demand has declined at a pace not seen since 2009 – how Has this impacted the business?

The decline in global graphic paper demand has been driven by a number of factors, including an economic slowdown in various parts of the world, the rapid series of price rises implemented in 2018 as a result of high paper pulp prices, and continuation of the secular impact of a shift from paper to digital. Additionally, in contrast to prior years when industry closures of higher-cost machines matched demand declines and kept operating rates high, in 2019 the pace of closure slowed. Further closures are only likely to occur in the second half of 2020. In response to the more than 10% reduction in demand for our major graphic paper products in the past year, we took 268,000 tons of production curtailment on our paper machines across the United States and Europe. The conversion of Somerset PM1 and Maastricht Mills in 2018 to paperboard grades helped lessen the impact of weak demand as we effectively reduced our graphic paper capacity by some 130,000 tons in the past year. As we ramp up in the coming year, this will further alleviate the impact from potential further declines in graphic paper markets. Market share gains in some grades helped our operating rates in the past year relative to the industry. Additionally, we started the review of our paper machines in Europe to determine whether and which paper machine we may need to close if the supply/demand imbalance in the industry remains. In North America, we plan to ramp up packaging volumes at Somerset Mill to relieve pressure from soft graphic paper demand.

Q: Governments and civil society are increasingly calling on business to do more to limit emissions and energy use to minimise climate change. What is Sappi doing in this regard?

Climate change, water scarcity, resource efficiency, minimising waste or pollution and job creation are key environmental, social and corporate governance (ESG) priorities for Sappi, albeit with different emphasis in different parts of the world. As a company that uses a renewable natural resource as raw material, we are faced with both opportunity and a duty of care in how we manage our operations and how we maximise the benefit or value we can derive from this resource while minimising the related costs or trade-offs. Although much of our energy generation and consumption is renewable, we still directly or indirectly depend on fossil fuels, particularly in South Africa. The investment at Saiccor Mill to expand capacity includes a change in technology that will allow us to recover more energy from our process and improve our water use efficiency. We are also investigating opportunities to improve energy efficiency at all our mills globally to improve our specific energy use and emissions. Unfortunately, in the last year, many of these metrics increased as lower graphic paper demand and downtime taken translated into a loss of efficiency as energy consumption does not decline linearly in these situations. The only solution to this challenge is to increase machine utilisation. Without a recovery in demand or significant market share gains, we may have to close a paper machine, which we are currently investigating as described above. In the coming year, we will be undertaking work in line with the global initiatives, Task Force on Climate-related Financial Disclosures (TCFD) and Science Based Targets (SBT) to better understand and quantify the risks and opportunities of climate change and what will be required to bring our long-term emissions profile in line.

Q: The strategic shift in capacity from graphic paper to packaging and speciality papers in the past year seems to have resulted in lower margins than previously indicated for that segment. Why is this?

The conversion from graphic papers to paperboard grades at Somerset and Maastricht Mills was technically successful, but the customer qualification and acceptance process took longer than originally envisaged. This has impacted the ramp-up of volumes and the mix of products sold. Lower operating rates and downtime related to the weaker graphic paper market also impacted negatively on raw material use and machine efficiency with related cost impacts. Lastly, high paper pulp prices at the start of the year and the low pulp integration levels of our packaging mills affected margins for much of the year. However, as pulp prices declined, we recorded a good improvement in segmental margins for the fourth quarter and the outlook in 2020 is for a sustained recovery in margins.

Sappi is a global diversified wood fibre company focused on providing dissolving wood pulp, packaging and speciality papers, graphic papers, as well as biomaterials and biochemicals to our direct and indirect customer base across more than 150 countries.

last week

4 years ago

2 weeks ago

last month

last month

3 months ago

4 months ago

4 months ago

5 months ago

5 months ago

Join WhatsApp Group

Join WhatsApp Group Join Telegram Channel

Join Telegram Channel Join YouTube Channel

Join YouTube Channel Join Job Channel (View | Submit Jobs)

Join Job Channel (View | Submit Jobs) Join Buy Sell Channel (Free to Submit)

Join Buy Sell Channel (Free to Submit) Paper News Headlines Channel (Free to read)

Paper News Headlines Channel (Free to read)