Join Groups & Channels, No Spamming

The BE and caustic soda plant marks a key milestone for Mohit Paper Mills, enabling full utilization of installed capacity and enhancing overall production efficiency

Expert Views on the paper market scenario, How the West Asia Crisis Helped the Industry, MIP for WPP, Anti-Subsidy implementation, and paper price trends

Pudumjee Paper intends to develop new varieties addressing applications for stronger paper bags and cupcakes; Plans 68,000 MT Mahad Specialty Paper Facility within 5 years

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

“Surging exports of paper will most certainly keep the domestic prices quite high”: Mr. A. Annamalai, Director – RFC

The Status of the Global Container board Industry, Recycled Paper Demand and Supply and its impact on the Indian Industry

Akshay Jain, director of Silverton Pulp & Paper, says it's time to promote agro residue as a raw material to lessen the scarcity of fibre

Advantageously located, a new paper mill is all set to roll kraft paper in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

TCPL Packaging navigates global challenges with strong domestic growth, Optimistic on export recovery and Rs. 100 crore capex in focus

TCPL Packaging navigates global challenges with strong domestic growth, Optimistic on export recovery and Rs. 100 crore capex in focus

Genus Paper continues to explore forward integration opportunities and diversify its portfolio to meet the growing demand for premium and specialty paper grades

Sardhana Paper Mill’s Expansion Reflects a Long-Term Vision Amid the Realities of India’s Kraft Paper Market

India Recommends Anti-Dumping Duty of Up to USD 376/MT on Virgin Multi-Layer Paperboard Imports from Indonesia

"We have to think unique and produce distinct items to remain in the business, Printers are stuck between manufacturers and customers", Says Kamal Chopra, President - AIFMP

Scientists from IIT-Guwahati develop India's first biodegradable plastic

“Paper Mills Transition from 'Made-to-Order' to 'Made-to-Stock' as Market Dynamics Evolve and the Allocation System Fades,” says Mr. Madhukar Mishra, MD, Star Paper Mills

Overview of exports of select type of paper and key raw material used in the industry by Crisil Intelligence

Margin pressure pushes Pulp & Paper Packaging sector toward AI-Driven cost optimization, Cutting costs by 8–20%

Michelman: Coating Solutions especially moisture and gas barrier on paper significantly improves the shelf life of food

The Pulp and Paper Times Magazine : Volume 6, Issue 1

The Pulp and Paper Times Magazine : Volume 5, Issue 6

The Pulp and Paper Times: Volume 4, Issue 6

The Pulp and Paper Times : Volume 3, Issue 6

The Pulp and Paper Times: Volume 2 Issue 5

The Pulp and Paper Times, Volume 1, Issue 3

The Pulp and Paper Times, November 2016 Issue

Kraft Paper Market: Current Scenario, Policy Impact, and Outlook for 2026

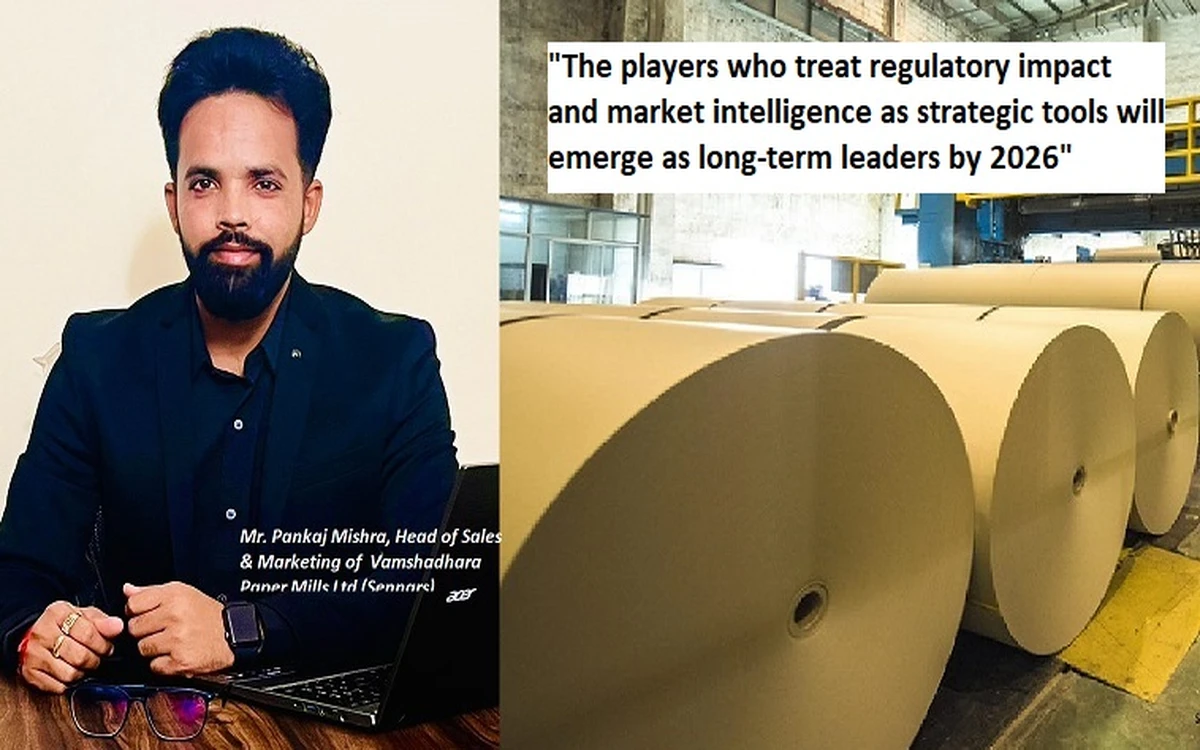

The article below is written by Mr. Pankaj Mishra, Head of Sales & Marketing of Vamshadhara Paper Mills Ltd (Sennars), specialises in kraft paper (both lower and higher gsm) and newsprint paper for diverse applications like packaging, printing, and publishing.

The Pulp and Paper Times

Over the past few years, the kraft paper industry has evolved from a conventional packaging segment into a critical component of the modern supply chain. Growing environmental awareness, the shift away from plastic packaging, and the rapid expansion of e-commerce and industrial packaging have significantly strengthened the demand for kraft paper. As the industry moves toward 2026, market dynamics will be shaped not only by consumption trends but also by taxation policies, tariff structures, and raw material availability.

Market Overview and Demand Trends

Kraft paper is widely used in corrugated boxes, cement and fertilizer bags, FMCG packaging, industrial wrapping, and logistics applications. Increasing restrictions on plastic usage and a strong push toward sustainable packaging solutions have positioned kraft paper as a preferred alternative across industries.

In emerging markets such as India, consistent growth in infrastructure projects, organized retail, and exports has supported steady demand. Additionally, recycled kraft paper has gained wider acceptance due to its cost efficiency and environmental benefits, further strengthening overall market volumes.

Raw Material Challenges and Cost Pressure

One of the key challenges for the kraft paper industry remains volatility in raw material prices, particularly waste paper and agro-based pulp. International waste paper prices are influenced by supply disruptions, import policies, and fluctuating freight costs, leading to frequent price uncertainty.

Energy costs—such as coal, power, chemicals, and water—also play a major role in determining production economics. By 2026, mills that invest in energy efficiency, captive power generation, and modernized machinery will have a clear competitive advantage. Smaller and technologically outdated units may face margin pressure unless they upgrade operations or adopt consolidation strategies.

Impact of GST Slab Changes

GST has a direct impact on pricing structures, working capital cycles, and cash flow management within the kraft paper industry. Any change in GST slabs affects manufacturers, traders, and packaging converters across the value chain.

An increase in GST slabs typically results in higher working capital blockage and puts pressure on demand, especially from small and medium-sized buyers. In such scenarios, passing on cost increases becomes difficult due to intense market competition, leading to margin compression for manufacturers.

Conversely, rationalization or reduction of GST slabs improves liquidity, supports demand growth, and encourages greater formalization within the industry. A stable and balanced GST framework by 2026 would enhance long-term growth prospects and reduce pricing distortions between organized and unorganized players.

Impact of Tariffs and Trade Policies

Tariff structures on imported waste paper, pulp, and finished paper products significantly influence domestic kraft paper pricing. Higher import duties protect domestic manufacturers, but they can also increase input costs if raw material availability within the country is insufficient.

Export-related tariffs and incentives are equally important. Supportive export policies can open new opportunities for Indian kraft paper in markets such as the Middle East, Africa, and South Asia. However, frequent changes in tariff regulations create uncertainty, making long-term capacity planning and pricing strategies challenging for manufacturers.

By 2026, a stable and predictable tariff regime will be essential for sustainable industry growth. Balanced policies that protect domestic production while ensuring access to affordable raw materials will determine the competitiveness of market leaders.

Shift Toward Quality, Technology, and Sustainability

The market is increasingly shifting its focus from volume-driven sales to quality-driven demand. Customers now expect consistent GSM, higher burst factor (BF), improved strength, and better printability. Mills investing in automation, real-time quality monitoring, and process optimization are gaining stronger customer confidence.

Sustainability has also become a decisive factor. Efficient water usage, effective effluent treatment, reduced carbon footprint, and compliance with environmental norms are no longer optional—especially for export-oriented businesses. By 2026, mills aligned with sustainability and ESG standards will enjoy better market acceptance and long-term pricing power.

Kraft Paper Market Outlook for 2026

By 2026, the kraft paper market is expected to witness steady growth with moderate price volatility. Demand from packaging, infrastructure, and export sectors will remain strong, while competition within the industry will intensify.

Manufacturers that proactively adapt to GST changes, tariff developments, and evolving customer requirements will be better positioned to manage risks and capitalize on opportunities. Investments in technology, cost efficiency, and long-term customer relationships will differentiate successful players from the rest.

In conclusion, the kraft paper industry is entering a more mature and disciplined phase. Growth will no longer depend solely on capacity expansion but on strategic decision-making, policy awareness, operational efficiency, and sustainability. The players who treat regulatory impact and market intelligence as strategic tools will emerge as long-term leaders by 2026.

1 days ago

Total Views : 287

4 days ago

Total Views : 454

5 days ago

Total Views : 382

last week

Total Views : 494

last week

Total Views : 892

last week

Total Views : 1080

last week

Total Views : 801

2 weeks ago

Total Views : 617

2 weeks ago

Total Views : 1551

2 weeks ago

Total Views : 935