India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

Satia Industries: better product mix and higher sales realization drive increased revenue in Q2FY23

CPPRI: Paper Industry contributes Rs. 8000 Crores to the National exchequer with a turnover of Rs.70000 Crores

“Surging exports of paper will most certainly keep the domestic prices quite high”: Mr. A. Annamalai, Director – RFC

Single-Use Plastic Ban: Everything, at each level, alternative for plastic will be expected from paper

The Status of the Global Container board Industry, Recycled Paper Demand and Supply and its impact on the Indian Industry

Akshay Jain, director of Silverton Pulp & Paper, says it's time to promote agro residue as a raw material to lessen the scarcity of fibre

Advantageously located, a new paper mill is all set to roll kraft paper in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

From FY 2010 to FY 2025, TCPL delivered a strong consolidated revenue CAGR of 16% and reported 31.18% export growth despite weak domestic demand

Indian Paper Industry under pressure; Mills announce multi-phase price revisions

Orient Paper and Industries revises capex plan, Approves 23,400 TPA new Tissue Machine at Amlai unit

“Paper mills are supplying at 0% GST but with a increased price to the extent of their Input credit loss,” says Mr. Shailendra Gala of Navneet Education

Paper Market scenario of WPP, Coated, and Packaging Boards, and MIP impact: Insights by Mr. Bhavesh Gala

"We have to think unique and produce distinct items to remain in the business, Printers are stuck between manufacturers and customers", Says Kamal Chopra, President - AIFMP

Scientists from IIT-Guwahati develop India's first biodegradable plastic

EBMA: With books exempt from GST, imported finished books enter India tax-free; notebook prices may climb 15–20% with GST hike

It is estimated that USD10B to USD20B worth of single-use plastic packaging will convert to molded fiber, ZUME

Muzaffarnagar gets a new capacity of Tissue Paper and MG Poster paper

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

Barrier-Coated Paper, RTE Demand, and E-Commerce: Experts Predict Paper-Based Packaging Market to Reach USD 46 Billion by 2030

BioCNG from paper mill effluent: India’s & Asia’s First Paper mill, Sainsons Paper to Produce & Sell CBG/BioCNG From Waste Water

Michelman: Coating Solutions especially moisture and gas barrier on paper significantly improves the shelf life of food

The Pulp and Paper Times Magazine : Volume 6, Issue 1

The Pulp and Paper Times Magazine : Volume 5, Issue 6

The Pulp and Paper Times: Volume 4, Issue 6

The Pulp and Paper Times : Volume 3, Issue 6

The Pulp and Paper Times: Volume 2 Issue 5

The Pulp and Paper Times, Volume 1, Issue 3

The Pulp and Paper Times, November 2016 Issue

Indian Pulp & Paper market scenario, import and export analysis, and emerging trends

Sluggish demand, oversupply, and cheaper imports are contributing to downward pressure on prices

The Pulp and Paper Times:

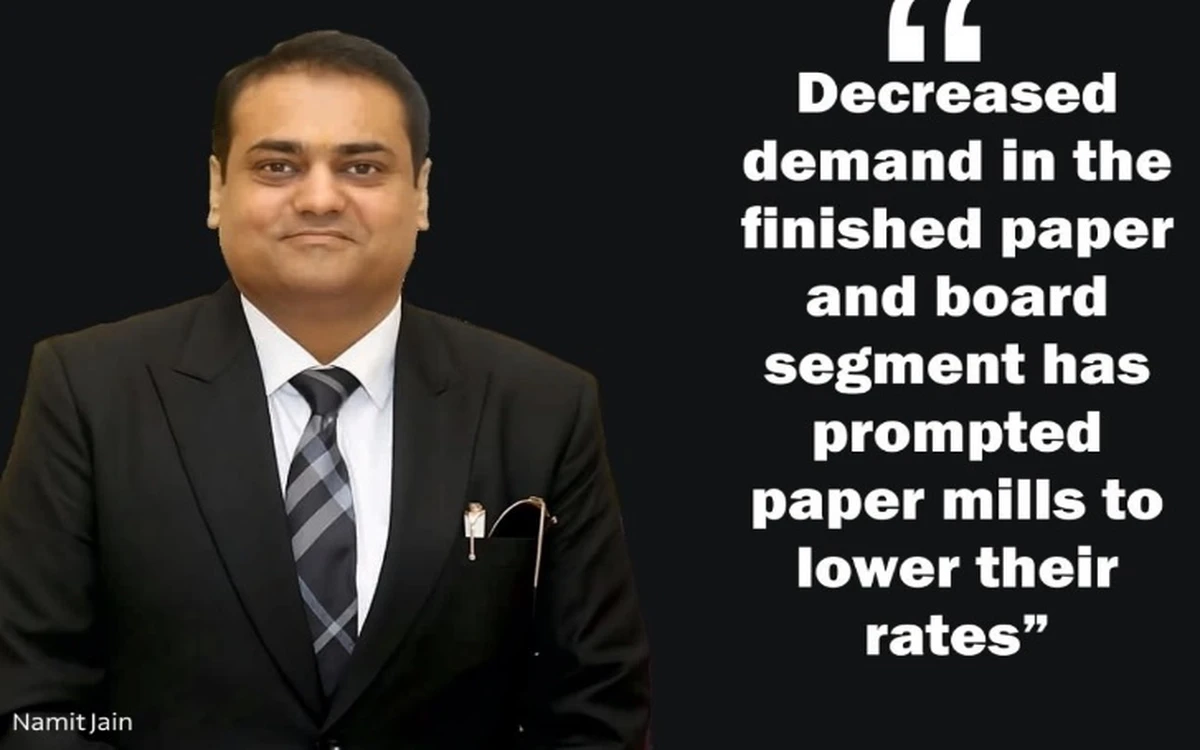

The current market conditions are characterized by sluggish demand, oversupply, and the availability of cheaper imports across various segments such as writing printing, packaging, and specialty products. These factors are contributing to a downward pressure on prices in the domestic market. Customers are hesitating to place new orders with dealers and paper mills due to this trend. Instead, they are selectively placing orders only for items that are experiencing shortages, exacerbating the situation. The decreased demand in the finished paper and board segment has prompted paper mills to lower their rates, leading to financial strain throughout the supply chain. This challenging situation appears likely to persist in the near future.

Export Scenario of WPP and other packaging grade paper:

Given the current situation, I personally can foresee a paper export demand slowdown over this quarter. Weak domestic demand in key economies such as China and the USA, along with the introduction of additional production capacities, has intensified competitive pressures in the export market. The combination of high shipping costs and trade agreements presenting significant hurdles in exporting, resulting in reduced sales volume and margins compared to previous years.

Paper Import Growth in various segments: reason and future anticipation:

The Indian paper industry has witnessed a notable rise in imports, particularly in the uncoated writing and printing segment and speciality grades. With major economies like the US and Europe facing economic downturns, international mills are turning to markets such as India. Trade dynamics and agreements from countries like Indonesia, Korea, Thailand is making import more attractive and prices defiantly a key driver for import of goods.

Indian mills have to look for three key drivers to compete with international mills which is quality, affordability and sustainability. Customers continue to prioritize quality, they also seek an enhanced experience at a reasonable price, particularly in light of the current inflationary conditions

Input Cost Analysis and pulp price scenario:

Currently it seems like the pulp industry is experiencing a period of oversupply, leading to inventory buildup and the closure of some production facilities. However, there are plans for new production units to come operational in the coming years, which will further increase the global supply of market pulp. The oversupply situation is expected to persist until there is a significant increase in demand, particularly from key economies like the US and China

Imported Waste Paper scenario:

The beginning of 2024 hasn't been favourable for India in recovered paper. Events such as the Red Sea complications, leading to increased freight costs, and delayed deliveries due to extended lead times have shifted the focus to the balance between movement and price as the primary factor for waste paper imports into the Indian market.

The supply from the USA is also in flux, with Openings of large-capacity mills utilizing recovered paper in the USA leading to a shortage of long fibre for export. This shortage has already driven up prices even before the Red Sea crisis, which has further exacerbated the situation.

Ocean freight rates for shipments of recovered fiber from the US East Coast to India have skyrocketed by US$400 per 20-foot container, resulting in an additional US$20 per tonne for the material. Delivery timelines for US shipments to India have stretched to 50-65 days.

Red Sea Crisis impact on domestic paper market | Mill and Traders:

The Red Sea Crisis, such as geopolitical tensions or disruptions in trade routes, can have significant implications for the domestic paper market, affecting both paper mills and traders.

Firstly, The shipping crisis in the Red sea has resulted in interruptions in the transportation of raw materials, including pulp and waste paper, to paper mills which lead to increase cost of production but these increased costs are not getting support in India due to the weak demand.

From the trader’s perspective we are facing challenges such as trade restrictions, market volatility, which is affecting pricing strategies and profit margins and moreover customers are looking for alternate suppliers from different geography.

ABOUT THE AUTHOR :

The above article on the present state of Indian Paper Industry is written by Mr Namit Jain, Director, HCSCJ Group & MTS Paper, HCSCJ a prominent player in the paper packaging market in Delhi since its establishment in 1951, began its export venture under the name MTS Papers India Ltd just before the COVID-19 pandemic hit India in 2020. Over the span of four years, we have expanded our base to Delhi and Dubai (MTS paper LLC-FZ). Our exports of papers and paperboards extend to over approx. 25 countries globally, with sourcing of paper materials from India, Far East, and Europe

Being a supplier for Writing Printing Paper & Packaging Boards, we consistently maintain robust and enduring relationships with both our customers and suppliers

just now

Total Views : 12618

just now

Total Views : 8187

just now

Total Views : 11240

just now

Total Views : 9368

just now

Total Views : 12030

just now

Total Views : 8907

just now

Total Views : 12913

just now

Total Views : 10188

just now

Total Views : 12628

2 weeks ago

Total Views : 10731

Join WhatsApp Group

Join WhatsApp Group Join Telegram Channel

Join Telegram Channel Join YouTube Channel

Join YouTube Channel Join Job Channel (View | Submit Jobs)

Join Job Channel (View | Submit Jobs) Join Buy Sell Channel (Free to Submit)

Join Buy Sell Channel (Free to Submit) Paper News Headlines Channel (Free to read)

Paper News Headlines Channel (Free to read)