Join Groups & Channels, No Spamming

Kuantum Papers achieved record paper sales volumes of 1,60,845 metric tonnes in FY 24–25; revenue stood at Rs. 1,113 crores; closed-loop automation through Project Nirmaan

Pakka Q3 FY26 conference call highlights stabilization of PM3, Progress in Jagriti Project, Strategic pause on US and Guatemala activities

Navneet Education to invest INR 100 crore annually over the next three years to unlock new growth across content publishing and supplementary segments

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

“Surging exports of paper will most certainly keep the domestic prices quite high”: Mr. A. Annamalai, Director – RFC

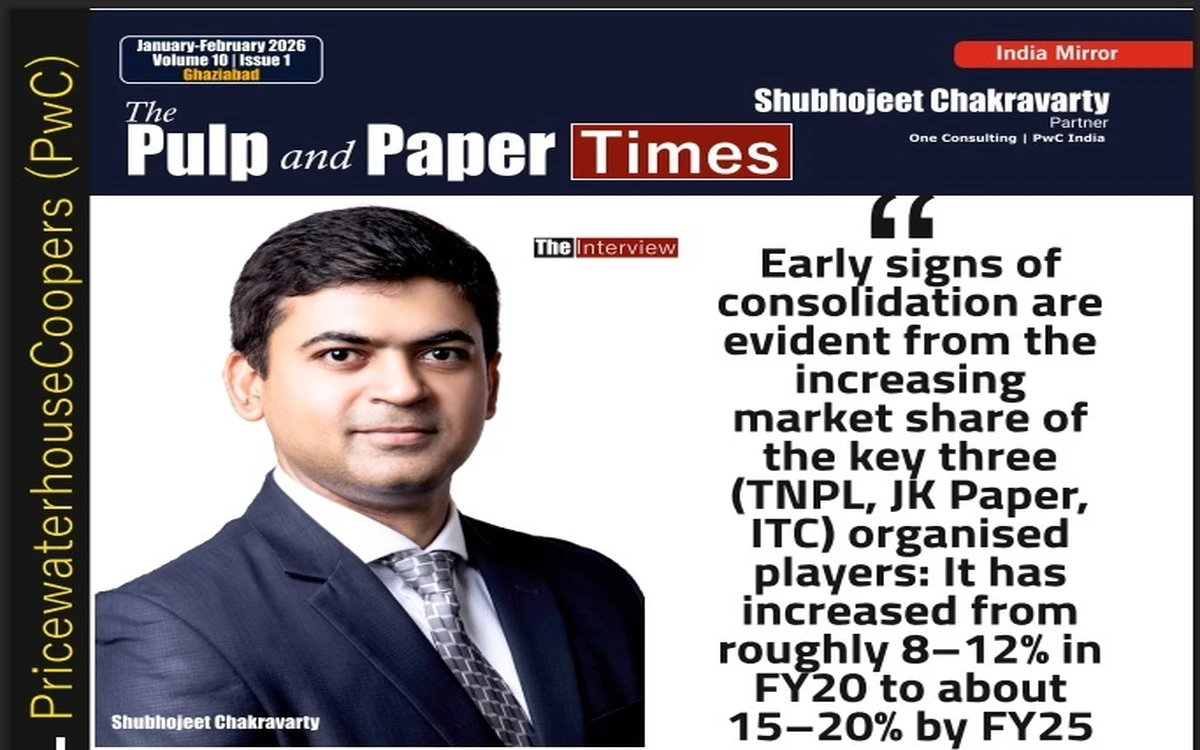

The Status of the Global Container board Industry, Recycled Paper Demand and Supply and its impact on the Indian Industry

Akshay Jain, director of Silverton Pulp & Paper, says it's time to promote agro residue as a raw material to lessen the scarcity of fibre

Advantageously located, a new paper mill is all set to roll kraft paper in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

Satia, Kuantum, Pudumjee, and West Coast released Q4 FY26 results; pricing improves on reduced dumping with a positive Q1 FY27 outlook, while TCPL’s Q4 profit drops 43%

Q3 FY26 Conference Call; TCPL Reports Revenue of INR 471 Crore with Improved Profitability, Falling Paper Prices Not Necessarily Negative for Packaging Sector

Q3 FY26 Conference Call; TCPL Reports Revenue of INR 471 Crore with Improved Profitability, Falling Paper Prices Not Necessarily Negative for Packaging Sector

Kuantum Papers achieved record paper sales volumes of 1,60,845 metric tonnes in FY 24–25; revenue stood at Rs. 1,113 crores; closed-loop automation through Project Nirmaan

Paper prices likely to adjust upward; Industry braces for massive impact in the coming months; ROCE below 8% insufficient for long-term growth: A.S. Mehta

"We have to think unique and produce distinct items to remain in the business, Printers are stuck between manufacturers and customers", Says Kamal Chopra, President - AIFMP

Scientists from IIT-Guwahati develop India's first biodegradable plastic

Overview of the Indian Education and Content Publishing Sector

JK Paper Strengthens Technology, Plantation and Packaging Strategy Amid Industry Challenges

BioCNG from paper mill effluent: India’s & Asia’s First Paper mill, Sainsons Paper to Produce & Sell CBG/BioCNG From Waste Water

Michelman: Coating Solutions especially moisture and gas barrier on paper significantly improves the shelf life of food

The Pulp and Paper Times Magazine : Volume 6, Issue 1

The Pulp and Paper Times Magazine : Volume 5, Issue 6

The Pulp and Paper Times: Volume 4, Issue 6

The Pulp and Paper Times : Volume 3, Issue 6

The Pulp and Paper Times: Volume 2 Issue 5

The Pulp and Paper Times, Volume 1, Issue 3

The Pulp and Paper Times, November 2016 Issue

Q. Paper Industry is a capital Intensive industry, The Cost of capital (Interest) is major a part of capital expenditure, Under COVID-19 situation, do you think that lockdown will eat out the liquidity of paper manufacturers? What sort of ‘help’ do you see from the government on this front?

The Covid-19 crisis has led to both supply and demand disruptions across most industries. As a result, companies have lost Revenues and Income while they continue to bear fixed costs, resulting in liquidity issues. Companies that are in the midst of expansion projects are going to suffer in terms of project delays and cost overruns, which will also adversely impact their cash flows.

Although the RBI has issued guidelines to banks on moratorium on loans, initially for three months, but later on it was extended till end of August, especially as the period under lockdown was also extended. There is a need to streamline the supply engines of the economy encompassing all the segments of the ecosystem - raw materials, inputs, intermediaries, logistics, distribution etc. as each of these has a cascading impact on the other. With people moving back to their villages and hometowns, labour shortage has become a significant disruptive factor in resuming operations after gradual unlocking of the economy since end-May/early June. Even if one assumes that these requirements are in place, Government’s role in stimulating demand in these tough times will be paramount. Producing without selling would mean nothing, especially if inventories keep rising. For example, at our plants, we have been gradually scaling up our capacity up to 75-80%. But we could not sustain it primarily due to demand issues, and have since scaled back to 65-70%.

With social distancing set to become the norm, even after the lockdown is over, consumers will remain apprehensive. This is more so as the spectre of job losses and the subsequent drying up of income will force postponement of discretionary purchases and limit spending to only necessities. It is crucial that the Government comes up with adequate safety nets as has been witnessed in several countries, both from the advanced world as well as emerging market economies

Different Industry associations have already made a lot of submissions to the Government with their ideas. Unlike the global financial crisis of 2008, Covid-19 is a natural disaster and for revival measures we need to look at it from disaster relief perspective.

Q Corona Epidemic has crippled the import of paper from China, The price of coated paper already increased in domestic market, how do you see this situation? The price of which paper grade may further be increased?

In the Coated paper segment, nearly 60% of the demand is met by imports. The supply chain disruptions following Corona virus pandemic affected the import of Coated paper from China. But at the same time, consumption has been limited during lockdown benefiting little to the domestic industry. However, Paper Mills in China are now fully operational and supply chain is slowly starting to normalize. In fact in near future as Chinese players face difficulty in marketing Coated paper elsewhere, they can divert Coated paper to India at a much lower price which will affect the domestic industry.

Besides Covid-19 crisis has led to an uncertain atmosphere which will impact the spending behaviour and habits of the consumer in the near future. Decisions on discretionary purchases will be postponed while trends such as work-from-home will shift consumption from away-from-home to at-home items.

Except for Food, Pharma packaging grades and certain hygiene products, most Paper grades will see only a gradual demand buildup and therefore may witness price pressure in the near future. In certain segments, e.g. recycled paper, raw material price spiked during lockdown due to challenges in waste paper collection and import consignments stuck at ports. However this was a temporary trend and reverse price movement has been observed lately.

Q. Indian Paper Industry has registered record profit in FY 18-19 and showing positive growth in their logbook despite increasing paper imports. How do you see this success of Indian paper mills in view of cheap paper imports?

India has enough capacity of Paper production except for categories such as Coated paper and Newsprint which are exposed to imports, which often come at low prices, thereby inhibiting new domestic capacity in these segments. The good profitability in FY19 was accompanied by favourable raw material price movements and significant effort by the industry to drive down cost along the value chain. While we may not have control over raw material price movement, competing against cheaper import will require Paper Industry to continuously drive efficiency gains and reduce cost. The role of favourable policy support , especially for plantations cannot be understated and therefore will be important for continued competitiveness of the Industry.

Q We are consuming paper at the rate of 1.6 Million MT per month according to IPMA, in almost 40 days lockdown, we may lose around 2 Million MT paper consumption. How important is this ‘data’ to Paper Industry, will this non-consumption bring unemployment in paper business?

The consumption loss may be lower than 2 Million MT as even during lockdown there was some consumption – maybe around 20-30% of normal levels. Moreover, no/meager supply during lockdown implies consumption loss is forever and industry is not going to recover the same.

A lockdown of over 50 days with limited production and little revenue generation has a massive impact on any business, and Paper Industry is no different. Since demand has been badly hit, even if the lockdown has lifted now, capacities will continue to remain under-utilized till the demand picks up. This would have consequences on the entire supply chain from channel partners and logistics service providers to suppliers of input materials.

Each Company will have to find its own way of dealing with this situation depending upon their value chain positioning and financial health. Some Companies may face survival challenges and may have to resort to even manpower cost reduction and workforce rationalization.

Q. If we evaluate the operation parameters of the Indian paper industry, which parameters propel the cost of paper production and make the Indian paper mills not competitive in comparison to foreign paper mills? How much paper industry is sensitive to make the paper mill operation optimized?

Today, Indian Paper Mills have some of the most technologically advanced Paper Machines. However, scale of operation plays a major role in determining unit economics across and this is one aspect which makes the domestic Mills less competitive than Global peers. This is a structural challenge that the Industry faces which may be difficult to overcome in short-to-mid term. Further, the cost of capital is also significantly higher in India and this adds to expense burden of the Paper Mills.

Paper Industry in India is getting sensitized to the need of efficient operations. We notice increasing investment in technologies that drive productivity, efficiency and sustainability. However we must diligently continue such efforts without losing focus - aggressive cost reduction and careful capex decision are key to ensuring long-term competitiveness. Additionally, issues like logistics and infrastructure, cost of capital, land and labour issues, multiple regulations need to be addressed to render Indian Industry to be competitive.

Q. According to Scientists that Corona Virus may come again as there is no vaccine developed for it, if it comes again, and the current situation emerges, What would you advice to Indian paper industry to survive?

While we are taking utmost care and following prescribed norms, a recurrence of virus is a real possibility, as seen in some South East Asian countries, even if it is beyond our zone of influence. We as an Industry have to show resilience and there is no way out other than facing and overcoming this calamity. Difficult situations require us to act differently and therefore the Indian Paper industry needs to continuously find newer ways of sustaining operations, servicing customers, rationalizing cost and up-skilling workforce. The Industry will be required to be more innovative in reducing cost of production. We must work closely with our channel partners and wherever applicable, support them through initiatives such as channel financing. We need to understand how the demand dynamics and consumer habits are changing and accordingly position ourselves to meet the emerging trends. The market is expected to remain volatile in near future and therefore proper planning will be key to avoid oversupply or stock-outs. In the last 3 months of Covid-induced lockdown, digital initiatives has gained further currency, with some trying out partnerships with e-commerce players to improve the last mile connectivity. Continuous learning and development initiatives towards capacity building will enhance knowledge, skill and self-efficacy of the workforce.

At JK Paper, we have cut down on non-essential costs, are continuously looking at newer channels to reach customers, have put greater emphasis on IT and are conducting various training programs for our employees.

Q. The rising paper cost will boost the sale of electronic gadgets and e-books which will impact the craze of paper in the long term thus paper industry may face saturation in the sale in the future. What are the long term plannings of Indian Paper Mills to counter the issue and maintain the growing demand for the paper?

The sale of electronic gadgets and e-books has had an impact on Graphic Paper market. The Global Graphics Paper market has witnessed a secular decline over the last 10 years during which the Newsprint segment declined at CAGR 6% while Printing & Writing (P&W) segment declined at CAGR 1.9%. This decline has a strong correlation with penetration of digital media. During the same period, in India, both Newsprint and Printing & Writing (P&W) segment witnessed a growth of CAGR 3% and CAGR 4-5%, respectively. However, lately, we have started witnessing slowdown in growth of Graphics Paper segment in India as well. And this trend is likely to accelerate with Covid-19 crisis as people are pushed to their homes and have to rely more on electronic communication thereby impacting demand from Corporate and Institutional buyers.

Over the last few years, we have witnessed closures and conversions of Graphics Paper capacity, globally. At some point in time, Graphics Paper market in India will also hit a plateau. Till then we must capture learnings from mature market, grasp consumer trends and reposition ourselves to embrace the future, through initiatives such as repurposing of assets, etc. This might lead to some consolidation. India remains one of the fastest growing markets in the Global Paper Industry and offers robust growth potential in Packaging, Tissue and Specialty segments. As such there is significant upside for the Industry to look up to.

13 hours ago

Total Views : 351

2 days ago

Total Views : 489

3 days ago

Total Views : 648

last week

Total Views : 841

last week

Total Views : 402

last week

Total Views : 748

last week

Total Views : 705

2 weeks ago

Total Views : 1086

2 weeks ago

Total Views : 812

3 weeks ago

Total Views : 1078