Navneet Education to invest INR 100 crore annually over the next three years to unlock new growth across content publishing and supplementary segments

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

Satia Industries: better product mix and higher sales realization drive increased revenue in Q2FY23

CPPRI: Paper Industry contributes Rs. 8000 Crores to the National exchequer with a turnover of Rs.70000 Crores

“Surging exports of paper will most certainly keep the domestic prices quite high”: Mr. A. Annamalai, Director – RFC

The Status of the Global Container board Industry, Recycled Paper Demand and Supply and its impact on the Indian Industry

Akshay Jain, director of Silverton Pulp & Paper, says it's time to promote agro residue as a raw material to lessen the scarcity of fibre

Advantageously located, a new paper mill is all set to roll kraft paper in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

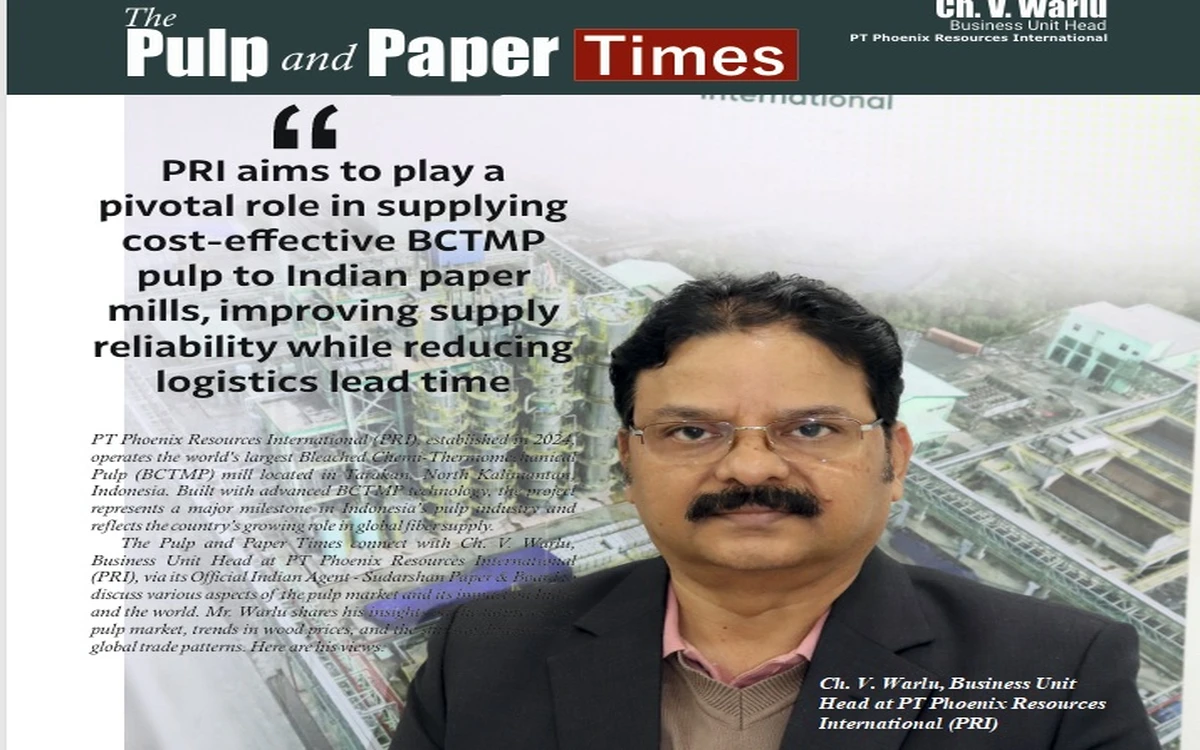

From Rs. 8,000 to Rs. 15,000 per tonne: wood cost surge hits paper industry margins; energy costs reshape outlook; relief expected by FY27–28: A.S. Mehta

Navneet Education to invest INR 100 crore annually over the next three years to unlock new growth across content publishing and supplementary segments

Paper prices push corrugated packaging costs up by 10–12%, while global logistics may take several weeks to stabilize even after the war ends: ICCMA President

Orient Paper and Industries revises capex plan, Approves 23,400 TPA new Tissue Machine at Amlai unit

Paper Market scenario of WPP, Coated, and Packaging Boards, and MIP impact: Insights by Mr. Bhavesh Gala

"We have to think unique and produce distinct items to remain in the business, Printers are stuck between manufacturers and customers", Says Kamal Chopra, President - AIFMP

Scientists from IIT-Guwahati develop India's first biodegradable plastic

EBMA: With books exempt from GST, imported finished books enter India tax-free; notebook prices may climb 15–20% with GST hike

It is estimated that USD10B to USD20B worth of single-use plastic packaging will convert to molded fiber, ZUME

Muzaffarnagar gets a new capacity of Tissue Paper and MG Poster paper

From Rs. 8,000 to Rs. 15,000 per tonne: wood cost surge hits paper industry margins; energy costs reshape outlook; relief expected by FY27–28: A.S. Mehta

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

BioCNG from paper mill effluent: India’s & Asia’s First Paper mill, Sainsons Paper to Produce & Sell CBG/BioCNG From Waste Water

Michelman: Coating Solutions especially moisture and gas barrier on paper significantly improves the shelf life of food

The Pulp and Paper Times Magazine : Volume 6, Issue 1

The Pulp and Paper Times Magazine : Volume 5, Issue 6

The Pulp and Paper Times: Volume 4, Issue 6

The Pulp and Paper Times : Volume 3, Issue 6

The Pulp and Paper Times: Volume 2 Issue 5

The Pulp and Paper Times, Volume 1, Issue 3

The Pulp and Paper Times, November 2016 Issue

Highlights

• Wood cost share rises from 40–45% to 50–55% of production cost

• Wood prices surge from Rs 8,000 to Rs. 15,000 per tonne in two years

• Overall cost impact estimated at ~10% increase

• Wood prices likely to ease significantly by FY27–28

In a detailed and structured address at an FPTA webinar on “Paper Market Today: Pricing, Supply & What’s Next,” Mr. A. S. Mehta, President of JK Paper Ltd., presented a comprehensive outlook on the paper industry, highlighting demand trends, cost structures, the impact of war, and the future trajectory of various paper segments.

Setting the context, Mr. Mehta emphasized the importance of analyzing the paper sector in a structured manner, identifying leading factors that provide clarity on future trends. He noted that while geopolitical developments, including the current war scenario, may have an impact, these remain short-term disruptions. “I would say this is a special or short-term impact,” he indicated, stressing that long-term fundamentals offer a clearer picture of the industry’s direction.

Cost Structure: Wood Remains the Dominant Factor

Turning to the cost structure of the paper industry, Mr. Mehta explained that raw material—particularly wood and pulp—continues to dominate the cost of production. He noted that nearly 45–50% of the total cost of production is attributed to wood or pulp.

For non-integrated players, where pulp is externally sourced, the cost of pulp alone can account for nearly 60% of total production cost. On the other hand, for integrated players, where wood is procured and processed internally, the wood cost typically accounts for around 50–55%, depending on location and logistics.

However, he pointed out that under normal circumstances, the wood cost component should ideally remain within 40–45% of total production cost. Over the past two and a half years, this share has significantly increased to 50–55%, reflecting a sharp escalation in wood prices.

“In the last two and a half years, the wood prices have gone up by almost 70–80%,” he stated. While the increase in wood prices is substantial, the overall impact on total cost structure is about 10%, which he described as “phenomenal” for the industry.

Wood Price Surge: From Stability to Sharp Escalation

Providing historical context, Mr. Mehta explained that wood prices remained fairly stable for nearly eight years. Between 2016–17 and the early 2020s, prices hovered between Rs. 6,500–Rs. 8,500 per tonne, with only minor annual inflation of 1–3%.

However, the scenario changed dramatically over the past two years. In FY24, prices began rising in the last two quarters, and by FY25, wood prices across the country surged from Rs. 8,000 per tonne to nearly Rs. 14,000 per tonne. In FY26, prices further increased to around Rs. 15,000 per tonne.

Thus, from a steady-state level of Rs. 7,500–Rs. 8,000 per tonne, wood prices nearly doubled to Rs. 15,000 per tonne.

Despite this sharp increase, Mr. Mehta noted that the industry has consciously avoided a drastic reduction in wood prices, even as supply conditions improve. Instead, prices have been gradually reduced by Rs.200–Rs.400 increments over the past six months, bringing current levels to around Rs. 13,000–Rs. 14,000 per tonne, depending on the mill.

Supporting Farmers Through Price Stability

Explaining the rationale behind this gradual correction, Mr. Mehta highlighted the importance of maintaining farmer confidence. During the period of high wood prices, farmers were encouraged to undertake large-scale plantation.

“If we would have reduced the wood prices drastically in a short period, farmers would have started uprooting the plantations,” he said.

To prevent this, the industry adopted a calibrated approach to price reduction, ensuring that plantation activity continues. Looking ahead, he expressed optimism that while FY26–27 may still witness relatively high wood prices, a significant correction is expected in FY27–28, which should provide relief to the paper sector.

Indonesia Forest License Revocations Impact Global Dynamics

Addressing a question on Indonesia, Mr. Mehta confirmed that several forest licenses have been revoked. In Indonesia, companies were operating under long-term forest concessions, allowing them to harvest wood at significantly lower costs.

However, issues such as lack of replantation, soil erosion, and even instances of improper practices led to the revocation of licenses for nearly 30 operators.

He contrasted this with India’s farm forestry model, which promotes sustainable plantation practices. For decades, Indonesian producers benefited from low-cost raw materials, enabling them to export paper at cheaper rates.

With the revocation of concessions, Mr. Mehta indicated that Indonesian producers are now likely to face higher wood costs, which could reduce their ability to dump low-cost products in international markets.

Understanding the Wood Cost Cycle

Mr. Mehta provided a long-term perspective on wood price fluctuations, stating that the industry experiences a cycle every 10 years, with 2–3 years of disruption caused by factors such as disease or external shocks.

In the current cycle, the COVID-19 pandemic played a critical role. Plantation activity was severely impacted during 2020 and 2021 due to lockdowns and disruptions during key monsoon seasons.

As plantation typically takes 2.5 to 3 years to mature, the reduced planting during the pandemic resulted in a shortage of harvestable wood in 2023–24, thereby tightening supply and driving up prices.

Additional Demand from Plywood and MDF Sectors

Another key factor contributing to the wood price surge was increased demand from plywood and MDF manufacturers. Earlier, these industries relied heavily on imported wood. However, with sufficient domestic availability, they shifted to local sourcing starting in 2022.

This coincided with reduced harvest availability, creating a demand-supply imbalance. Mr. Mehta noted that this combination “played havoc” with wood prices.

He further explained that wood cost constitutes over 80% of production cost for plywood and MDF manufacturers, compared to 50–55% for paper companies. As a result, these industries also faced significant profitability pressures.

Encouragingly, both sectors have now begun investing in plantation and resuming imports, which, along with increased plantation by paper companies since 2022, is expected to improve wood availability in 2026 and beyond.

Wood Varieties and Optimization Strategies

Responding to a query on wood quality, Mr. Mehta explained that paper mills use a mix of wood varieties such as eucalyptus, subabul, and casuarina, depending on fiber properties, cost, and regional availability.

Eucalyptus offers better brightness, while subabul and casuarina are preferred for easier cooking due to their softer fiber. Mills optimize the mix based on cost efficiency and desired pulp characteristics.

He also highlighted the role of agroclimatic conditions. For instance, casuarina is more suitable for coastal regions, while subabul may not be preferred in states like Odisha. Proximity to mills and transportation costs further influence wood selection.

Energy and Chemical Costs Add Pressure

Apart from wood, Mr. Mehta identified energy costs as a major concern for the paper industry. Coal availability remains inconsistent, as priority allocation by Coal India is often given to the power sector.

During periods of shortage, paper mills are forced to procure coal from the open market or import it, leading to higher costs. The situation worsens during monsoon months, when mining operations are disrupted and coal quality deteriorates due to moisture.

He noted that while the coal situation had improved briefly, it has again become challenging in recent months.

Chemical costs have also shown significant volatility. For example, caustic soda prices, which were around Rs. 25 per kg, have surged to Rs. 35–Rs. 40 per kg in recent months. Similarly, starch prices remain unstable due to competing industrial demand.

“These are some of the cost implications which are impacting the industry,” he observed.

Conclusion: Cost Pressures and Cyclical Recovery Ahead

Mr. Mehta’s address provided a clear and data-driven understanding of the cost dynamics shaping the paper industry. While short-term disruptions such as war may influence pricing and supply, the core challenges lie in raw material costs, energy availability, and cyclical supply constraints.

The sharp rise in wood prices—driven by pandemic-related plantation gaps and increased cross-industry demand—has significantly altered the cost structure. However, with plantation activity picking up and supply improving, a gradual correction is expected over the next two years.

At the same time, volatility in coal and chemical prices continues to add pressure, making cost management a critical priority for industry players.

Overall, the outlook suggests that while the paper industry remains on a steady growth path, navigating input cost fluctuations and ensuring sustainable raw material supply will be key to maintaining profitability in the years ahead.

4 minutes ago

Total Views : 12209

4 minutes ago

Total Views : 12166

4 minutes ago

Total Views : 10626

4 minutes ago

Total Views : 12676

4 minutes ago

Total Views : 9346

4 minutes ago

Total Views : 12267

4 minutes ago

Total Views : 11335

4 minutes ago

Total Views : 12169

4 minutes ago

Total Views : 8419

4 minutes ago

Total Views : 12140

Join WhatsApp Group

Join WhatsApp Group Join Telegram Channel

Join Telegram Channel Join YouTube Channel

Join YouTube Channel Join Job Channel (View | Submit Jobs)

Join Job Channel (View | Submit Jobs) Join Buy Sell Channel (Free to Submit)

Join Buy Sell Channel (Free to Submit) Paper News Headlines Channel (Free to read)

Paper News Headlines Channel (Free to read)