Navneet Education to invest INR 100 crore annually over the next three years to unlock new growth across content publishing and supplementary segments

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

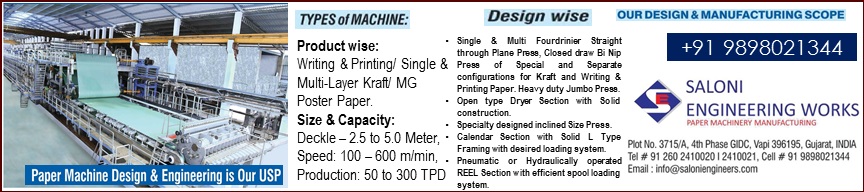

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

Satia Industries: better product mix and higher sales realization drive increased revenue in Q2FY23

CPPRI: Paper Industry contributes Rs. 8000 Crores to the National exchequer with a turnover of Rs.70000 Crores

“Surging exports of paper will most certainly keep the domestic prices quite high”: Mr. A. Annamalai, Director – RFC

The Status of the Global Container board Industry, Recycled Paper Demand and Supply and its impact on the Indian Industry

Akshay Jain, director of Silverton Pulp & Paper, says it's time to promote agro residue as a raw material to lessen the scarcity of fibre

Advantageously located, a new paper mill is all set to roll kraft paper in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

Balaji JMC Paper Mill: The first Indian paper mill in Mexico completes twelve months of commercial production, with sell-through yield consistently tracked above 92%

Navneet Education to invest INR 100 crore annually over the next three years to unlock new growth across content publishing and supplementary segments

Paper prices push corrugated packaging costs up by 10–12%, while global logistics may take several weeks to stabilize even after the war ends: ICCMA President

Orient Paper and Industries revises capex plan, Approves 23,400 TPA new Tissue Machine at Amlai unit

Paper Market scenario of WPP, Coated, and Packaging Boards, and MIP impact: Insights by Mr. Bhavesh Gala

"We have to think unique and produce distinct items to remain in the business, Printers are stuck between manufacturers and customers", Says Kamal Chopra, President - AIFMP

Scientists from IIT-Guwahati develop India's first biodegradable plastic

EBMA: With books exempt from GST, imported finished books enter India tax-free; notebook prices may climb 15–20% with GST hike

It is estimated that USD10B to USD20B worth of single-use plastic packaging will convert to molded fiber, ZUME

Muzaffarnagar gets a new capacity of Tissue Paper and MG Poster paper

“Every parcel shipped anywhere in the world has strengthened the demand for packaging board, corrugated boxes, protective papers, and specialty grades,” said Pavan Khaitan at Paperex

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

BioCNG from paper mill effluent: India’s & Asia’s First Paper mill, Sainsons Paper to Produce & Sell CBG/BioCNG From Waste Water

Michelman: Coating Solutions especially moisture and gas barrier on paper significantly improves the shelf life of food

The Pulp and Paper Times Magazine : Volume 6, Issue 1

The Pulp and Paper Times Magazine : Volume 5, Issue 6

The Pulp and Paper Times: Volume 4, Issue 6

The Pulp and Paper Times : Volume 3, Issue 6

The Pulp and Paper Times: Volume 2 Issue 5

The Pulp and Paper Times, Volume 1, Issue 3

The Pulp and Paper Times, November 2016 Issue

Key Points of Interview:

“PRI maintains operational flexibility to meet diverse customer specifications and evolving product requirements”

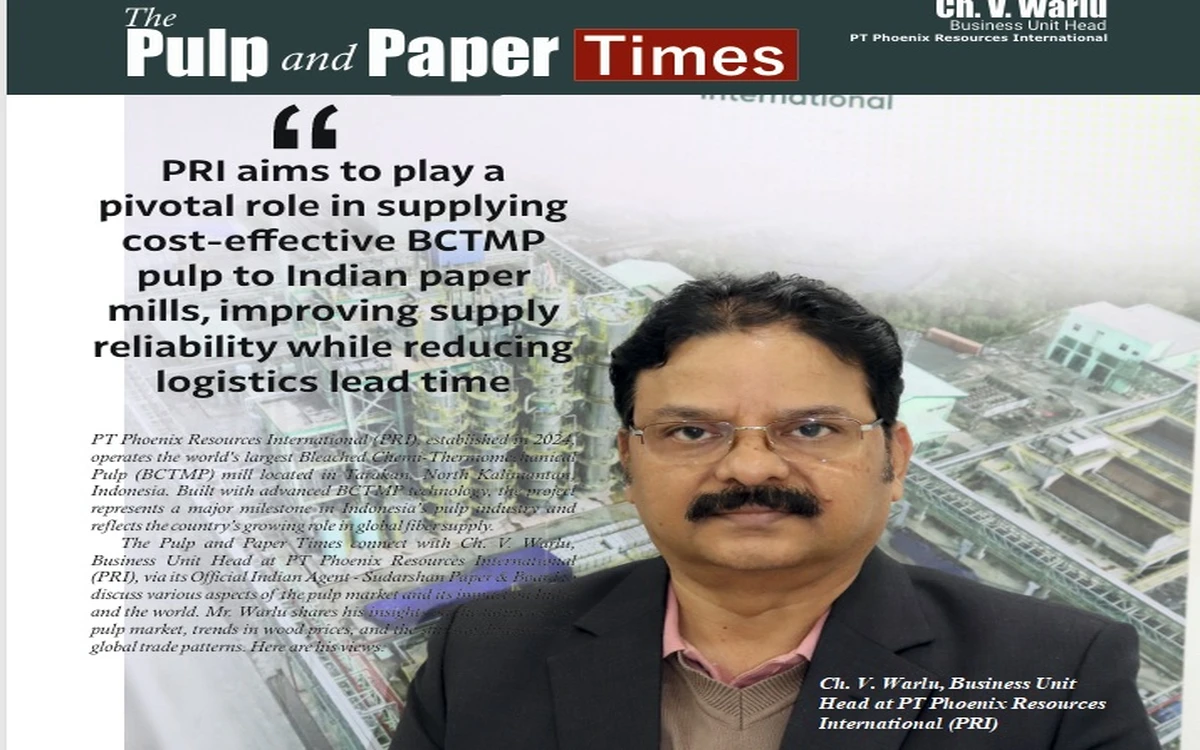

“PRI aims to play a pivotal role in supplying cost-effective BCTMP pulp to Indian paper mills, improving supply reliability while reducing logistics lead time”

“Pulp will be stronger in 2026 and sustain the year with substantial upside as compared to 2025”

PT Phoenix Resources International (PRI), established in 2024, operates the world’s largest Bleached Chemi-Thermomechanical Pulp (BCTMP) mill located in Tarakan, North Kalimantan, Indonesia. Built with advanced BCTMP technology, the project represents a major milestone in Indonesia’s pulp industry and reflects the country’s growing role in global fiber supply. The Pulp and Paper times connect to Ch. V. Warlu, Business Unit Head at PT Phoenix Resources International (PRI) via its Official Indian Agent - Sudarshan Paper & Board, discusses various aspects of the pulp market and its impact on India and the world. Mr. Warlu shares his insights on the future of the pulp market, trends in wood prices, and the shifting dynamics of global trade patterns. Here are his views:

The Pulp and Paper Times

Q: Could you briefly outline PT Phoenix Resources International’s (PRI) journey and its current position in Indonesia’s pulp industry?

PT Phoenix Resources International (PRI), established in 2024, operates the world’s largest Bleached Chemi-Thermomechanical Pulp (BCTMP) mill located in Tarakan, North Kalimantan, Indonesia. Built with advanced BCTMP technology, the project represents a major milestone in Indonesia’s pulp industry and reflects the country’s growing role in global fiber supply.

The integrated facility includes:

• Wood handling capacity of 8,900 GMT per day

• A 192 TPD peroxide plant

• A desalination plant producing 32,000 m³ of fresh water daily sustainably.

• A dual-unit captive power plant generating 2 × 150 MW

Beyond industrial scale, the project reflects PRI’s commitment to sustainable development. The desalination system significantly reduces dependence on local freshwater resources, helping protect surrounding ecosystems while supporting community water security. Our plantations are well aged and give access to matured fiber having 6 + years average age , which makes our quality standout.

PRI is positioned not only as a large-scale pulp producer but also as a catalyst for regional economic development, job creation, and responsible industrial growth, demonstrating that innovation and environmental stewardship can progress together.

Q: How do you analyze the current market scenario of pulp? How do you see the next 3–6 months for WPP and pulp segments?

BCTMP prices during 2025 experienced volatility, with both hardwood and softwood grades facing pressure due to oversupply from Western part of the world. Since Q4-2025, however, hardwood pulp prices have recovered steadily.

Looking ahead to the next 3–6 months, prices are expected to remain firm to moderately stronger, supported by:

• Gradual demand recovery in China

• Tightening inventories

• Stable packaging and board demand in Asia

Market dynamics could shift further if one or two hardwood BCTMP mills in Canada undergo permanent shutdowns.

Many large board and printing & writing mills are increasingly integrated with APMP lines and import BCTMP primarily for premium grades, export orders, and certification requirements such as FSC, PEFC, or EUDR compliance. Although this segment is smaller, it remains strategically important.

PRI’s geographic proximity to India and other Asian markets provides logistical advantages and improved supply reliability for regional customers.

Q: India is focusing on plantation development amid rising wood costs. How does PRI evaluate India’s fiber situation compared with Indonesia, and does Indonesia have a cost advantage?

India continues to face a structural wood-fiber deficit, with domestic supply often lagging behind growing demand. While several leading Indian producers have made commendable investments in plantations, a significant portion of the industry still depends on Agro-forestry systems, which face challenges in consistency, yield, fiber maturity and long-term scalability.

The most critical constraint remains land availability and high population density as agricultural, residential, and industrial demands limit large-scale plantation expansion. This restricts fiber security and increases cost volatility for Indian mills.

Indonesia presents a strong contrast. The country benefits from:

• Decades of plantation management expertise

• Advanced silviculture and genetic improvement programs

• Highly mechanized forestry operations

• Large-scale land availability for sustainable plantations

• Access to aged wood from plantations ageing 6 + years

These advantages enable exceptionally high yields per hectare and stable wood supply, resulting in a structurally more competitive wood cost base. Consequently, Indonesian pulp producers are able to offer consistent quality, reliable supply, and cost competitiveness — creating a clear strategic advantage in global markets.

Q: What is PRI’s current pulp production capacity and product portfolio? Are there expansion or modernization plans?

PRI currently operates with an annual production capacity of approximately 800,000 tons of pulp, primarily focused on hardwood BCTMP.

The company works closely with customers to optimize furnish design for both board and paper applications, delivering cost-effective fiber solutions without compromising performance or quality. PRI maintains operational flexibility to meet diverse customer specifications and evolving product requirements.

Q: Do you foresee long-term supply agreements between Indonesian producers and Indian paper mills becoming more common?

India’s paper and packaging sector is expanding rapidly, driven by growth in e-commerce, FMCG, and education. However, domestic pulp production remains limited and relatively high cost, making imports essential.

In this context, PRI sees strong potential for long-term strategic supply partnerships with Indian mills. Such agreements help ensure supply continuity, quality stability, and reduced exposure to price volatility — creating sustainable value for both suppliers and customers.

Q: With fluctuations in global pulp prices, how should Indian paper mills plan their sourcing strategy?

Wood cost accounts for nearly 70% of paper production cost, making fiber security critical. A balanced mix of domestic fiber development and strategic imports will remain essential for long-term stability.

Indian mills should focus on long terms relationship and engagement with sustainable suppliers in terms of cost , quality , technology and scale . Quarterly contracts can help them beat volatility to some extent.

Q: How do you view the trade relationship between Indonesia and India in pulp & paper, and PRI’s role in this market?

India currently imports BCTMP largely from distant geographies, while domestic production is limited to a few integrated mills serving captive requirements.

A significant demand–supply gap continues to exist. With its proximity to India and strong fibre security, PRI aims to play a pivotal role in supplying cost-effective BCTMP pulp to Indian paper mills, improving supply reliability while reducing logistics lead time.

Q: How do you see the pulp market evolving after EUDR implementation?

The European Union Deforestation Regulation (EUDR) will introduce stricter compliance requirements and higher traceability standards. While this may increase operational costs, it will accelerate the transition toward transparent and sustainable supply chains.

Producers capable of demonstrating deforestation-free sourcing with precise geolocation data will gain competitive access to European markets. PRI has already aligned its operations with EUDR requirements and views compliance as a long-term opportunity rather than a constraint.

Q: How do you foresee pulp and paper market growth in 2026 amid Chinese market slowdown and global overcapacity?

Despite moderation in China’s paper market, demand growth in India, Southeast Asia, and emerging economies continues to support overall consumption. Packaging grades remain structurally strong due to e-commerce and FMCG expansion.

While global overcapacity may create short-term pricing pressure, efficient producers with secure fiber resources and strong cost structures are expected to remain resilient. Pulp will be stronger in 2026 and sustain the year with substantial upside as compared to 2025.

Q: Do you foresee strategic shifts in India toward agro-residue pulp or recycled fibre usage?

India possesses abundant agro-residues such as wheat straw and bagasse, which support sustainability goals and help reduce dependence on wood fibre.

However, large-scale adoption faces challenges including fragmented collection systems, fiber quality variability, and environmental compliance requirements. Rising wood costs and imports of low-priced paper are encouraging some mills to increase recycled fibre usage, particularly in packaging grades.

A balanced fiber mix combining recycled fibre, agro-residue, and imported virgin pulp will likely define India’s future furnish strategy.

Q: What message would you like to share with global buyers and paper manufacturers?

PRI is committed to serving customers with high-quality hardwood BCTMP pulp through long-term, sustainable partnerships. Our focus remains on delivering reliable supply, consistent performance, and environmentally responsible fiber solutions that support our customers’ growth in an evolving global market.

just now

Total Views : 11039

just now

Total Views : 12323

just now

Total Views : 9853

just now

Total Views : 10670

just now

Total Views : 12033

just now

Total Views : 8803

just now

Total Views : 9457

just now

Total Views : 8365

just now

Total Views : 11886

just now

Total Views : 9705

Join WhatsApp Group

Join WhatsApp Group Join Telegram Channel

Join Telegram Channel Join YouTube Channel

Join YouTube Channel Join Job Channel (View | Submit Jobs)

Join Job Channel (View | Submit Jobs) Join Buy Sell Channel (Free to Submit)

Join Buy Sell Channel (Free to Submit) Paper News Headlines Channel (Free to read)

Paper News Headlines Channel (Free to read)