Join Groups & Channels, No Spamming

The BE and caustic soda plant marks a key milestone for Mohit Paper Mills, enabling full utilization of installed capacity and enhancing overall production efficiency

Expert Views on the paper market scenario, How the West Asia Crisis Helped the Industry, MIP for WPP, Anti-Subsidy implementation, and paper price trends

Pudumjee Paper intends to develop new varieties addressing applications for stronger paper bags and cupcakes; Plans 68,000 MT Mahad Specialty Paper Facility within 5 years

India Paper Industry at an Inflection Point: War, Costs, and Capacity; Demand growth expected at 5–7% in FY26

A new capacity in Tissue and specialty paper mfg.; Machine Design, Installation, and commissioning by Saloni Paper Machines

“Surging exports of paper will most certainly keep the domestic prices quite high”: Mr. A. Annamalai, Director – RFC

The Status of the Global Container board Industry, Recycled Paper Demand and Supply and its impact on the Indian Industry

Akshay Jain, director of Silverton Pulp & Paper, says it's time to promote agro residue as a raw material to lessen the scarcity of fibre

Advantageously located, a new paper mill is all set to roll kraft paper in Madhya Pradesh

Several agile interventions helped ITC-PSPD fortify its clear leadership of the Value Added Paperboards (VAP) segment

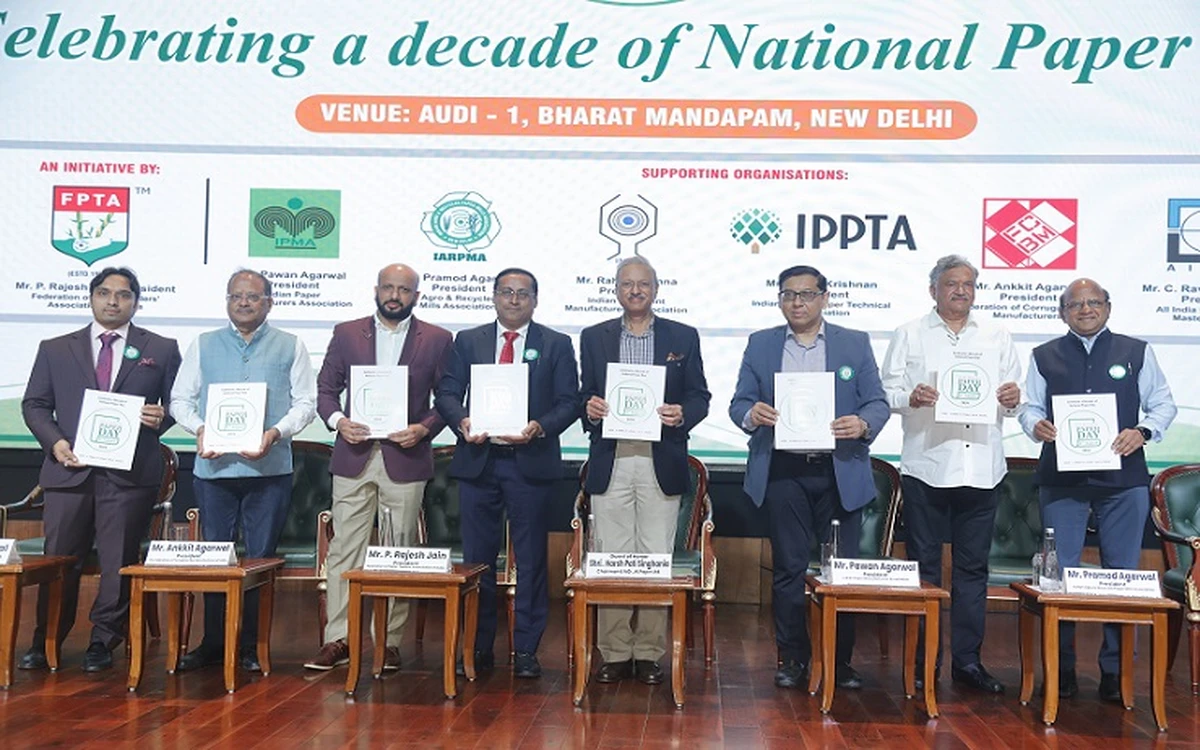

Seven Leading Associations Unite to Celebrate National Paper Day, Highlighting Paper's Sustainability and Circular Economy Advantage

Seven Leading Associations Unite to Celebrate National Paper Day, Highlighting Paper's Sustainability and Circular Economy Advantage

Seven Leading Associations Unite to Celebrate National Paper Day, Highlighting Paper's Sustainability and Circular Economy Advantage

Navneet Education focuses on brand building, curriculum-led growth, and export recovery; expects stationery margins to improve in FY27

Sardhana Paper Mill’s Expansion Reflects a Long-Term Vision Amid the Realities of India’s Kraft Paper Market

India Recommends Anti-Dumping Duty of Up to USD 376/MT on Virgin Multi-Layer Paperboard Imports from Indonesia

Scientists from IIT-Guwahati develop India's first biodegradable plastic

Navneet Education focuses on brand building, curriculum-led growth, and export recovery; expects stationery margins to improve in FY27

It is estimated that USD10B to USD20B worth of single-use plastic packaging will convert to molded fiber, ZUME

Muzaffarnagar gets a new capacity of Tissue Paper and MG Poster paper

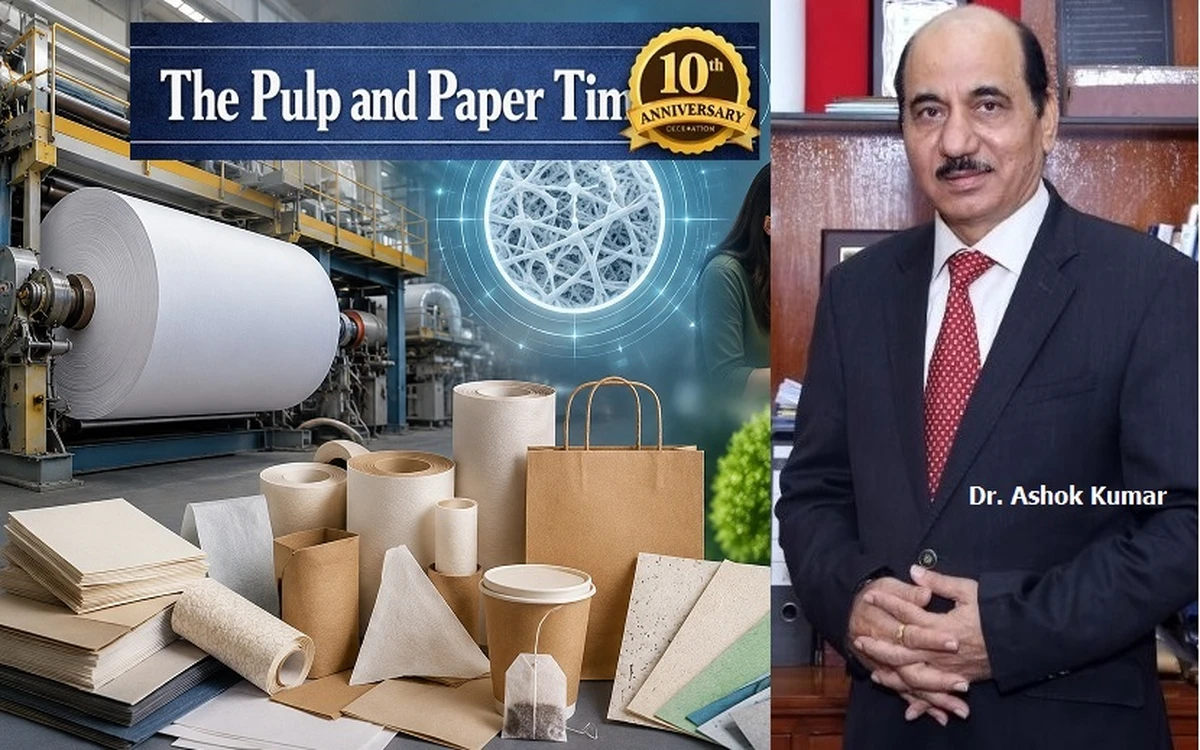

Speciality Paper Manufacturing: Market Factors, Technology, and Consumer Interests by Dr. Ashok Kumar, ED – Pudumjee Paper

Overview of exports of select type of paper and key raw material used in the industry by Crisil Intelligence

Margin pressure pushes Pulp & Paper Packaging sector toward AI-Driven cost optimization, Cutting costs by 8–20%

Michelman: Coating Solutions especially moisture and gas barrier on paper significantly improves the shelf life of food

The Pulp and Paper Times Magazine : Volume 6, Issue 1

The Pulp and Paper Times Magazine : Volume 5, Issue 6

The Pulp and Paper Times: Volume 4, Issue 6

The Pulp and Paper Times : Volume 3, Issue 6

The Pulp and Paper Times: Volume 2 Issue 5

The Pulp and Paper Times, Volume 1, Issue 3

The Pulp and Paper Times, November 2016 Issue

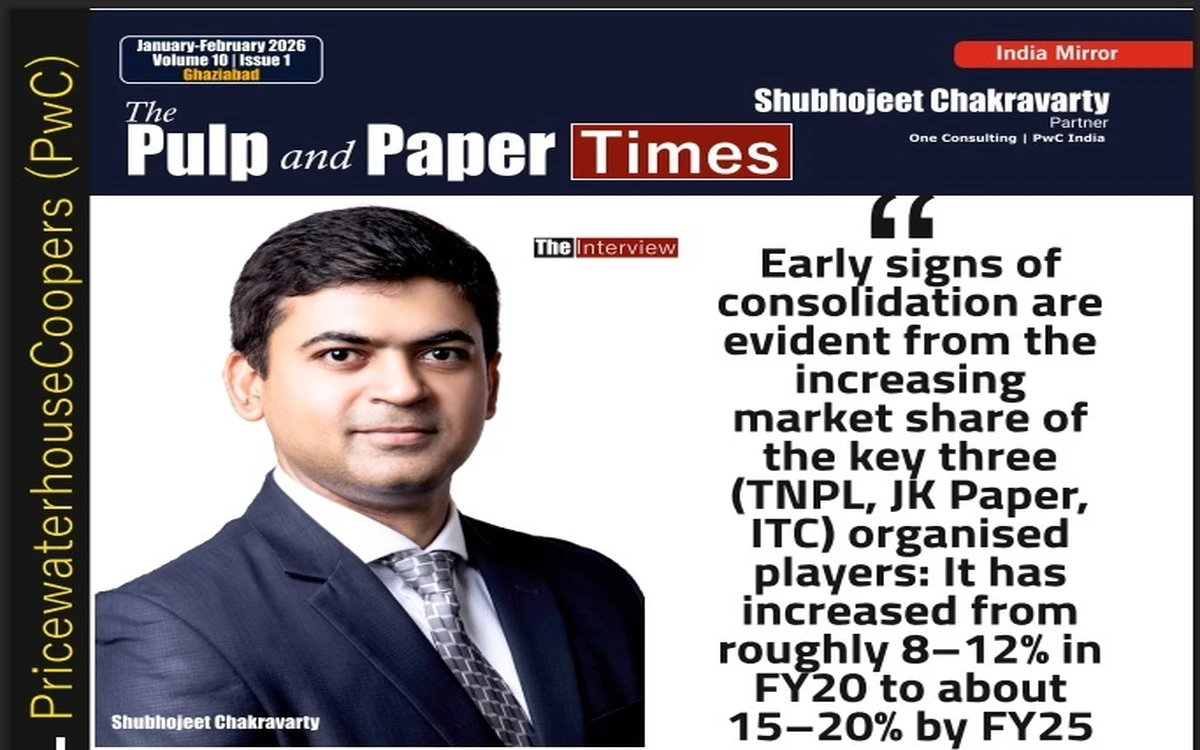

Key Points of the Interview:

-Early signs of consolidation are evident from the increasing market share of the key three (TNPL, JK Paper, ITC) organised players: It has increased from roughly 8–12% in FY20 to about 15–20% by FY25

-Currently, 240 out of 800 paper mills in India are non-operational.

-Currently, integrated mills having an in-house pulp manufacturing facility could enjoy a cost advantage of 20–30% in case of BHKP and 35–45% in case of BCTMP over paper and paperboard mills dependent on import of pulp

-The MIP offers only short-term support, as it applies to a few grades and is valid for a limited period. Once it ends, lower-priced imports may return and add pressure on domestic prices

-Large integrated mills already contribute about 30% of national output and have the capital and scale to further integrate.

-In contrast, India is enhancing sustainability through circular practices, while China prioritises environmental performance through scale, technology, and strict enforcement.

-Capacity expansion in recent times has added significant supply, and this is softening sales realisations, especially in packaging grades.

In an exclusive conversation with The Pulp and Paper Times, Mr. Shubhojeet Chakravarty, Partner | One Consulting – Capital Projects & Infrastructure, PwC India Private Limited, delves into the intricate challenges and opportunities within the Indian paper industry. He sheds light on the growth of the pulp and paper sector in India, current market conditions, future trends, Impact of Minimum Import Price, and the availability of fiber. Additionally, Mr. Chakravarty highlights the compound annual growth rate of domestic paper demand and shares his invaluable insights into the nuanced landscape of the industry. Here is his full interview.

The Pulp and Paper Times

Q: Please give a brief introduction to PwC.

At PwC, we help clients build trust and reinvent so they can turn complexity into competitive advantage. We’re a tech-forward, people-empowered network with more than 364,000 people in 136 countries and 137 territories. Across audit and assurance, tax and legal, deals and consulting, we help clients build, accelerate, and sustain momentum.

For the paper and packaging sector in India, PwC has supported diversified clientele with both strategy formulation and implementation. Our works include business transformation programs covering people, processes, technology and assets. These interventions have delivered tangible outcomes such as higher domestic sales volumes, improvements in plant throughput, reduction in operating costs, and sustained profitability gains.

Q. How do you evaluate the current market conditions for Indian paper manufacturers, specifically in the writing and printing paper (WPP), board, and packaging segments, given that margins are shrinking?

Over the past year, the Indian paper and paperboard market has witnessed steady demand but rising supply pressure. Capacity additions have become operational. while global paper prices remain subdued, creating a supply heavy environment. Competitive imports have further constrained pricing power, particularly in commodity grades.

WPP is growing at an annual growth rate of 2–3% in India, which is higher than global levels. This can be attributed to the rising literacy rate in Tier-II and Tier-III cities. Raw material cost increased by 20–25% in last 2 years due to supply constraints, and mills have struggled to pass on cost increases due to cheap imported copier and printing grades. Writing and Printing Paper (WPP) margins have reduced sharply and are expected to be under pressure this year as well due to import competition and elevated wood costs.

Paperboard and packaging contribute more than 55% of industry revenues. The growth of packaging paperboard at an annual rate of 8–10% is primarily driven by the growth in sectors such as FMCG, pharma, retail, and e-commerce. However, the segment faces intense pricing pressure due to increased imports from ASEAN and China.

Board manufacturers face margin erosion due to high wood/pulp costs, inverted duty structure combined with cheap imported board. Despite strong demand, profitability is expected to remain weak this year. Going forward, scale, integration, and product mix upgrades will be critical for margin resilience.

Q. What impact do you see the imposing of Minimum Import Price (MIP) on virgin multi-layer paperboard (MLP) and GST 2.0 having on the margins in the current FY?

The MIP aims to provide stability by preventing sharply discounted virgin multilayer boards from China and ASEAN countries (especially Indonesia) from entering the domestic market during a period of global oversupply. This helps maintain sales realisations and supports utilisation for domestic players.

While MIP offers some protection to realisations, GST 2.0 introduces a structural profitability challenge. The GST rate applicable to base grades such as uncoated paper and paperboard used for writing and printing increased from 12% to 18%, while the rate for exercise books and notebooks decreased from 12% to 0%. Similarly, the rate for cartons and boxes also decreased from 12% to 5%, creating an inverted duty structure for the converters. As the converters accumulate excess input credit under this framework, they resist any upward price revisions, which means manufacturers are unable to pass through increases in fibre, energy, or chemical costs even when their input costs become more expensive.

As a result, GST 2.0 compresses margins for segments linked to educational and corrugated packaging chains. For several manufacturers, analysing product mix realignment becomes very important to offset the margin pressure.

Q. What structural changes do you think the Indian paper industry has undergone during the last 5 years w.r.t. consolidation, technology adoption, and capacity expansion?

The Indian paper industry has observed significant structural changes in the last five years. Industry consolidation has accelerated, with large, organised players strengthening their positions through acquisitions. ITC’s acquisition of Century’s paper business and APRIL Group’s acquisition of a controlling stake in Origami reflect an increasing trend of acquisition by large domestic and global players. Early signs of consolidation are evident from the increasing market share of the key three (TNPL, JK Paper, ITC) organised players: It has increased from roughly 8–12% in FY20 to about 15–20% by FY25. Additionally, small/mid-sized players have struggled due to volatility of pulp prices and reduced prices for imported paper/paperboard. This has led to the suspension of operations by around 130 paper mills in North India, while 20 out of 100 paper mills have shut down in Gujarat in the last two to three years. Currently, 240 out of 800 paper mills in India are non-operational.

Technology adoption is becoming a key differentiator for large and organised players. Leading players are upgrading ERP systems and evaluating advanced automation and smart factory technologies. One area where we have seen the change is adoption of high quality and semi-automated machines by mid-sized players, which was earlier limited to large-scale players only. On the other hand, large players are focusing on improving productivity, product quality, and supply chain efficiency through data analytics and integration of technology platforms.

Selected large and mid-sized players are expanding capacity across the value chain. Companies such as ITC and JK are not only increasing existing capacity but also diversifying into new product segments. They are setting up new pulp mills to strengthen supply chain control and to mitigate risks associated with pulp price volatility and currency fluctuations. In contrast, most Indian players continue to focus primarily on expanding capacity within their existing finished‑goods lines, with limited diversification. A notable emerging trend, however, is the growing interest among paper manufacturers in the production of agro‑based and bamboo‑based pulp and associated products. This shift is particularly aimed at serving high‑growth markets such as tableware and tissue manufacturing, where demand for sustainable and alternative fibre sources is rising. In addition, various players are planning or expanding capacity in the coated paper segment.

Q. Is the Indian paper industry’s packaging segment expected to see sustainable growth?

This segment is likely to experience growth due to structural demand. The Indian paper packaging market is projected to grow at a CAGR of 8–10% in the next 5 years. This growth is supported by the growth in multiple sectors such as e-commerce, quick commerce, food and beverage, personal care, pharma, premium FMCG, and FMCD.

The Indian paper-based packaging segment is expected to see sustained growth, driven by the substitution of plastic with fibre-based materials. The transition towards sustainability is driving the reduction of plastic usage. Increasing regulatory restrictions on single-use plastics, coupled with corporate commitments to circular packaging, are significantly broadening the market for recyclable paper-based solutions. This is particularly evident in the demand for corrugated boxes, folding cartons, and aseptic liquid packaging boxes.

Global brands are innovating with fibre-based flexible packaging. It shows how premium packaging is moving toward biodegradable materials. In India, this shift is also visible through ITC’s Filo range, which uses fibre-based, food-safe board with specialised paper coatings to replace plastic in takeaway and disposable packaging. These innovations reflect the shift in demand toward fibre-based materials.

Companies such as Pakka, Chuk, and Ecoware are scaling biodegradable packaging and moulded fibre tableware made from bagasse and agricultural residue, indicating a long-term commitment to sustainability.

Q. How do you see India’s per-capita consumption rising by 2030?

The projected domestic consumption of paper and paperboard for FY25 is around 23.5 million tonnes per annum. At a 5% CAGR, demand is projected to reach about 30 million tonnes by 2030. The per capita paper consumption is expected to rise from approximately 16 kg (FY25) to around 19–20 kg (FY30). This increase will be driven by strong demand from the FMCG, e-commerce, and food services sectors.

Q. How is the Indian paper industry achieving the goal of carbon neutrality by 2050? What steps would you suggest for achieving this?

The Indian paper industry is gradually moving towards carbon neutrality using cleaner energy and alternative raw materials. Manufacturers are now shifting from the use of conventional fossil fuels to biomass and renewable power, which helps lower direct emissions. The use of agro residue, recycled fibre, and plantation of wood is rising as consumer preference for sustainable packaging increases and brands push suppliers to lower their footprint.

Wider use of renewable energy, advanced chemical recovery, logistics optimisation, and increase in alternative-fibre sourcing require investment in the right technology. Firms should focus on achieving energy efficiency through scale, retrofitting dryers/steam recovery systems, investing in Zero liquid Discharge (ZLD) systems, and process improvement. These steps also help reduce fuel, raw material, and quality-related operational costs, which are essential for manufacturers facing sustained pricing pressure and competition from imports.

The introduction of the Carbon Credit Trading Scheme (CCTS) is expected to give a strong boost to decarbonisation efforts in the pulp and paper industry, which is one of the nine sectors included under the Compliance Mechanism. This mechanism creates a market-driven reward for deeper emissions reductions, by allowing those that outperform their targets to earn tradable carbon credits.

Under the scheme, the pulp and paper industry is required to meet phased greenhouse gas (GHG) emission intensity reduction targets for 2025–26 and 2026–27, with cuts of up to 15% considering FY24 as baseline.

Q. Is the Indian paper industry expected to leapfrog towards domestic pulp manufacturing, agro-residue pulp or plantation model? What’s your viewpoint?

With demand expected to grow at a CAGR of around 5%, the raw material gap will further widen, increasing the urgency for domestic capacity creation. India currently uses a diverse range of fibre sources, including wood, recycled paper, and agricultural residues. However, it remains significantly susceptible to global pulp price fluctuations. Limited availability of fibrous wood resources, alongside a reliance on imported pulp, has led to an increasing exploration of alternative fibre sources by various mills.

The Indian paper industry is unlikely to follow one fibre model. It is expected to move gradually across domestic wood pulp and agro-residue pulp options.

Domestic wood pulp manufacturing is expected to expand because integrated mills gain clear cost benefits while also reducing exposure to pulp price volatility, foreign exchange risk, logistics disruptions, and geopolitical uncertainties. Currently, integrated mills having an in-house pulp manufacturing facility could enjoy a cost advantage of 20–30% in case of Bleached Hardwood Kraft Pulp (BHKP) and 35–45% in case of Bleached Chemi-Thermo Mechanical Pulp (BCTMP) over paper and paperboard mills dependent on import of pulp. These savings make integration attractive, although high capital costs and the requirement of water and fibre could slow such adoption.

Large integrated mills already contribute about 30% of national output and have the capital and scale to further integrate. SMEs lack modern pulping capability. Integrated players are most likely to build domestic pulp lines as a hedge against global price volatility.

Agro-residue pulping units are growing where bagasse and wheat straw are available, supporting niche applications and innovative products like moulded fibre tableware. However, yields are lower, functional performance varies, and raw material quality is inconsistent. These issues prevent the rapid substitution of wood-based paper.

Plantation forestry will remain a critical long-term driver, but progress depends on land availability, farmer partnerships, crop cycles, and adoption of yield improvement techniques (such as clonal production). Overall, the shift will remain gradual, with each model growing where fibre availability and economics support it.

Q. From sustainability and pricing perspective, how do Indian paper manufacturers differ from Chinese paper manufacturers?

Indian paper manufacturers and Chinese manufacturers differ mainly in dependency on raw material, scale, cost, and sustainability practices. India’s industry is fragmented, with a few large mills and many small and unorganised players.

India operates a multi‑fibre model—wood, agro‑residue, and recycled paper with import dependency. In contrast, Chinese manufacturers rely heavily on virgin wood pulp. Large-scale, integrated wood-pulp operations provide China with better control over fibre quality. This also leads to higher costs and uneven efficiencies. China operates large, integrated, and capital-intensive mills. These factories produce consistent quality at lower unit cost, which helps them compete strongly in global markets.

China has progressed faster on sustainability, supported by well-organised recyclable paper collection systems, and deployment of modern and high-efficiency machines. It also has strict environmental compliance, resulting in the rapid shutdown of non-compliant mills. It leads the world in large, efficient pulp mills that use advanced recovery boilers, low energy, and high automation.

However, its reliance on virgin pulp raises land-use concerns. In contrast, India is enhancing sustainability through circular practices, while China prioritises environmental performance through scale, technology, and strict enforcement.

Q. Considering the expected oversupply in FY25/26 and FY26/27, how will the profit margins of the paper industry be impacted in the next few years?

India has already been facing oversupply pressures due to a surge in imports from China and ASEAN, which made India a net importer. The paper industry is likely to face margin pressure over the next two to three years. Capacity expansion in recent times has added significant supply, and this is softening sales realisations, especially in packaging grades. Imports are expected to stay competitive because global prices remain weak, which limits pricing power for domestic players. The MIP offers only short-term support, as it applies to a few grades and is valid for a limited period. Once it ends, lower-priced imports may return and add pressure on domestic prices. Smaller and non-integrated mills are supposed to feel the impact first due to higher fibre and energy costs. Integrated players with integrated pulp may remain better protected. To manage margins, manufacturers may plan to reduce energy use, plan raw materials carefully, and improve logistics efficiency. Overall profitability will stay tight until demand absorbs the added capacity.

Q. What is your viewpoint on the future of the Indian WPP segment?

The WPP segment in India is expected to continue its steady growth at the rate of around 2–3% per annum, even as global demand continues to soften. In India, consumption remains supported by government educational initiatives and rising literacy rates in rural areas (including Tier-II and Tier-III cities). However, long-term growth will be hindered because digital usage is rising across urban nodes. Digitisation poses a long-term threat to this segment and moderates its growth by 2–3%. Moreover, pricing remains under pressure since the inverted tax structure for convertors limits the ability of paper manufacturers to pass on cost increases.

As a result, manufacturers are now exploring capacity augmentation by adding coating units to their existing WPP production line. This helps them shift part of their production towards higher-value coated papers such as NCR paper, thermal paper, and kaolin-coated paper. These grades offer better margins and allow diversification without large new investments.

Q. How significant is the impact of EU Deforestation Regulation (EUDR) on the Indian graphic paper and pulp market?

EUDR applies to all wood-based products, including printing and writing paper, graphic paper, pulp, books, cartons, and packaging substrates. This regulation establishes compliance obligations for all Indian producers exporting to the EU, particularly those involved in graphic paper, wood-free paper (WFP), specialty paper, and market pulp. This will have a meaningful impact on India’s graphic-paper and pulp exports because it raises the standard on traceability. It mandates exporters to provide clear origin data and supply-chain documentation. Small manufacturers may find it challenging to meet the documentation and geolocation requirements, which could limit access to EU buyers. For larger and integrated players, the EUDR presents both a cost and an opportunity, as those who invest in backward integration can gain credibility and retain high-value European customers. However, compliance will depend heavily on the location strategy of mills. Sourcing must come from areas where land records, plantation boundaries and farmer clusters can be mapped and verified. Fibre also needs to be procured from nearby regions, as long-distance sourcing raises logistics costs and weakens competitiveness.

Indian mills will need significant updates in supply-chain transparency, such as raw material tracking, certification systems, and digital chain-of-custody platforms. These updates will increase costs and complexity.

Q. How is your organisation helping Indian paper companies gear up for digital transformation and ESG compliance?

Support for digital and ESG adoption is becoming central for Indian paper manufacturers, and the focus is shifting from point solutions to full value-chain strengthening. We support businesses in assessing operational baselines, including fibre sourcing, energy use, logistics efficiency, and process improvement. We also help in building digital roadmaps that introduce smart factory initiatives, ERP upgrades, and plant-level automation. We support on logistics optimisation (e.g. control‑tower visibility, network redesign) to reduce operational cost, increase profitability, and improve service levels.

From an ESG perspective, we support clients in identifying material ESG priorities relevant to the paper sector, including emissions measurement, fibre traceability, water and energy efficiency, and evaluation of alternative fibre options. This is complemented by a dedicated initiative focused on structured ESG and impact reporting, helping clients clearly articulate sustainability outcomes to investors and stakeholders. Our work also covers ESG governance, investor-readiness support (including ESG ratings and benchmarks), compliance with emerging regulations, and climate-risk assessments for assets. This integrated digital ESG approach helps mills improve margins, reduce risk, and become future-ready.

Q. How do you foresee the growth of the paper industry in FY25/26 and FY26/27?

The industry is expected to grow at a moderate pace of 4–5% in FY25–26 and FY26–27, supported mainly by steady demand in packaging paper and boards. FMCG, pharma, food delivery, and retail will continue to drive consumption, while tissue and specialty grades will expand from a low base. However, recent capacity additions will keep the market supply-heavy, softening realisations across several grades even if volume growth remains stable. Imports will also remain competitive as global prices stay subdued. The recently introduced MIP may offer brief protection in select grades, but its impact will be temporary and not sufficient to materially change the demand–supply balance. Integrated players with lower fibre costs are likely to capture a larger share of incremental demand, while smaller mills may face margin pressure.

Q. Do you have any message for the Indian paper industry?

The Indian paper industry is entering a phase where competitiveness will increasingly depend on cost advantage, technology adoption, and sustainable fibre security. Demand fundamentals remain strong. However, pricing pressure from imports and rising input costs requires a sharper focus on operational efficiency, integration, and product diversification. As global markets move decisively toward traceable and low-carbon materials, Indian manufacturers need to strengthen supply-chain transparency and invest in cleaner energy. The message is simple: Companies that take proactive steps today in digital adoption, ESG readiness, and product mix planning will be best positioned to capture long-term growth and build resilient, globally competitive businesses.

Now is the time to focus on innovation, the development of alternative fibres, and improving scale efficiencies. Global regulations like the EUDR should be viewed as an opportunity to create traceable supply chains with low deforestation risk, positioning India as a sustainable and reliable global supplier. The future will belong to mills that can demonstrate their sustainability credentials rather than just make claims.

For Indian companies, the key to success lies in collaboration rather than competition. Firms should work on developing common traceability platforms, unified advocacy for FTA corrections and GST adjustments, and shared research and development into agro-fibre pulping, bamboo, and circular systems.

8 hours ago

Total Views : 915

16 hours ago

Total Views : 5123

3 days ago

Total Views : 3114

5 days ago

Total Views : 4112

6 days ago

Total Views : 2098

last week

Total Views : 1677

last week

Total Views : 3667

last week

Total Views : 2204

last week

Total Views : 583

last week

Total Views : 2604